2019 bit the dust and what a year it was. With all the political ups and downs, it would have been hard to come up with the script.

So how would we describe the Golf market in 2019? In footballing parlance, I think it would be “a season of two halves”.

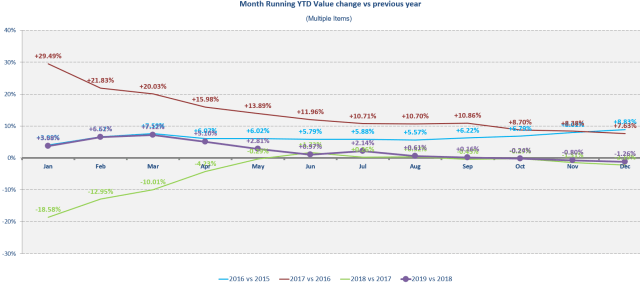

The first half saw the market get off to a roaring start. In March, we were over 7% up YTD and things were looking good. May was okay but then it all started to unravel the following month: one of the worst Junes for a long time which saw 80% more rain than average. We hoped this was a blip but, little did we know, it was a sign of things to come.

The second half of 2019 saw 20% more rain than normal. And, sadly, the net result was a market down more than 1%* on 2018. Actually a similar trend to 2018 on 2017.

Was it all doom and gloom?

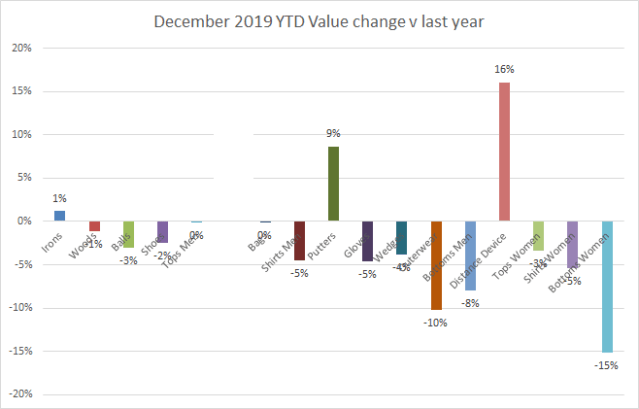

In reality, 2019 ended up a mixed bag. While most categories were down, there were a few upsides. Overall market value was down about 1.2%. Among the categories monitored by the Golf Datatech UK retail audit, 3 were up, 2 were flat and 11 were down. I have ignored Trolleys from these stats as we have made a change in the model this year that throws the trends off a bit. Interestingly the biggest category, Irons, saw growth.

Overall, there was a confused performance among the main categories with Clubs up (just), Apparel down quite a lot, and Consumables also struggling.

At the start of last year I was hoping that we were going to see some growth. I was still positive in June, even though this had been a very poor month. Unfortunately, this was not the case and the year limped to slight decline.

Having studied a few more trends, I can now say that the writing was perhaps on the wall, even in June. Looking at the last 8 years, 4 saw a percentage drop in year on year total sales from mid year to year end of between -2% and -4%. Two years were static and 2 saw slight growth. So, in most instances, things don’t tend to trend upwards from mid year.

Here are the trends for the last 4 years:

Going forward, it is pretty safe to assume that the half year result is probably the best case scenario and is more likely to be followed by a small decline, especially if the market is up at mid-year.

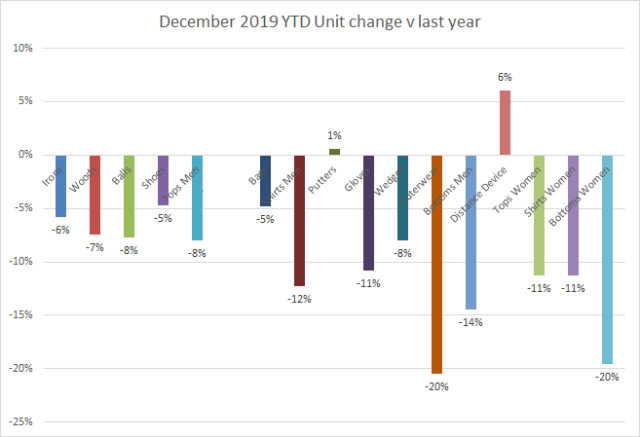

How about Units?

We saw a similar trend to previous years in unit sales – general decline across most categories. Putters and Distance devices did grow. However, they were the only plus points.

In unit terms the 14 other categories declined between -5% and -20% with Outerwear being the worst affected.

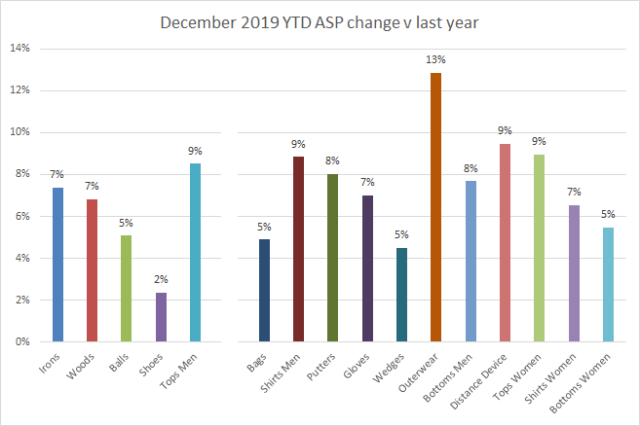

And Asp’s?

When it comes to Average Selling Prices (ASP’s), we had a trend first! This was the first year that all 16 tracked categories saw an increase in price. Smallest was Shoes at 2%, largest was outerwear at 13%.

Were classic price and demand economics at play? Price goes up, unit sales goes down? I am not so sure. In some categories, it would appear that could be the case – the increase in ASP of Woods, Irons, Tops and Bags is directly in line with the decrease of units: that’s 4 of the tops 6 categories. Perhaps there is some price sensitivity here. But if you look at the 2 markets that grew in value this year, both had large price increases and some unit increase (even thought Putters was small). I think price is having an effect but the overall poor performance is down to other elements.

Did price increases put a dampner on the market?

My hunch is that a number of factors had an effect. The economy has been negatively impacted by political uncertainty and this impacted growth. General retail had a rocky year. The Brexit confusion and a general election left everyone scratching their heads as to what is going to happen and probably led to wallets remaining firmly in pockets. At least things now appear to be moving forward with some certainty. We have left the EU.

While we are not seeing macro growth through a buoyant economy right now, all things considered, the Golf market has fared relatively well. Looking at the general sales mix, two of the categories that grew are high value items: Irons and Distance devices. This leads me to think that people were willing to spend money – if they weren’t you would expect the more expensive categories to have taken a hit. This wasn’t the case.

In contrast, Balls and Gloves (relatively low value items) were both down On Course roughly -5% in units, (Off course was even more). While prices have gone up it shouldn’t have been enough to impact sales. So I would think this has to indicate that less people were playing or consuming these items, meaning less golf being played and less people in the store. And less money spent.

So why might participation have been down? If you look at the weather, the second half of the year had 20% more rain than average. We also had more, what I call, rain days: days with more than 1mm of rain. In fact I think we probably lost over 2 weeks of golf when compared to the average. Rain had an impact but I believe weather apps are also having affecting behaviour. Yes, mobile phones might be impacting the Golf industry. I have heard a number of anecdotes saying that players haven’t gone golfing because the app forecast rain. This might also explain why even with the bad weather Outerwear was significantly down.

What does all this mean for 2020?

I was hoping for some growth last year. I think I said 3% at the beginning. It’s a shame that didn’t work out especially as my record of prediction has been pretty good to date.

For 2020, I think we’ll hope for some growth – again. Why? Well the general mood feels better than it has recently. I think the UK will start moving forward again, now the act of leaving the EU is done – even though the details haven’t been worked out. The Golf product at the PGA show looked good in Orlando and so suppliers will spend more money on promotion. The Off Course sector is in better shape to allow for some hopeful year on year comparisons. The football champs this year are likely to hit June and July but those months last year were so poor, I don’t think they can be much worse.

There are, however, two curve balls at the moment: the weather and the Corona virus. Weather usually has more of an impact on the year at the start, so we’ll keep an eye on this. If we can get off to a good start, growth has a chance. However the Corona virus is presently an unknown. Is it going to lead to travel and shipping issues for all. Will it be contained or will it cause further anxiety and panic. While a number of patients have sadly died, it is worth remembering that over 10,000 people have died in the US from the flu this season and that hasn’t hit the news at all.

Lets be positive and hope the sun comes out and they find a cure for the virus. If not then I will have to revise my position come May!

As always, I’m happy to help and answer any questions you might have on the market data, so do send any thoughts or queries, across to me.

For more information about Golf Datatech’s retail audit data, covering all the key golf categories in the US, UK, Sweden, Germany and France, contact Phil at pbarnard@golfdatatech.com