June 2021 was another big month for golf retail in the UK. Here’s another quick video update with more stats.

June 2021 was another big month for golf retail in the UK. Here’s another quick video update with more stats.

With the challenges that have been thrown our way, it’s no mean feat for retailers to have made it half-way through 2021. Lockdown lows followed by pent-up booms and a smattering of Euro football to boot! With ‘freedom day’ now been and gone, we’ve officially been released, so let’s take a few minutes to review how we’re doing so far during this crazy year.

2021 started off with less of a bang and more of a slammed door. Golf, and pretty much everything else in the country, was closed for 3 months and, while Lockdown 2.0 took its toll on liberties, how much did it effect the overall golf economy?

Interestingly, the impact wasn’t as bad as Lockdown 1.0 which we can attribute to three things:

1 – In the UK, the start of the year is the smallest time of year for the golf economy, so the effect of closed golf shops will have a reduced consequence on total sales.

2 – The weather wasn’t great so, while people couldn’t get out to play, they probably didn’t want to anyway.

3 – Retailers, both On- and Off-Course, were far more prepared to shut down and more inventive when it came to selling their wares, while still abiding by the rules.

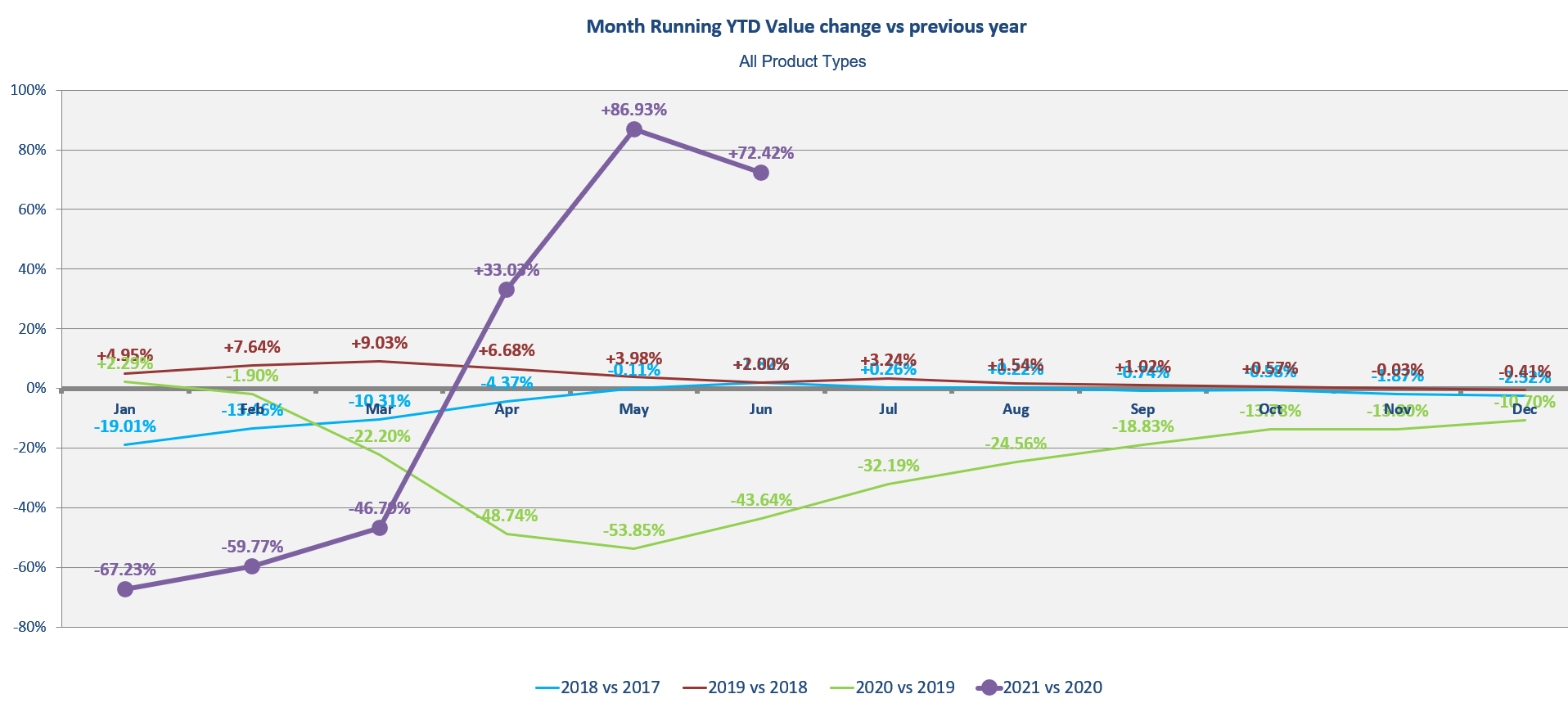

While the totals looked bad, (the market was down 47% year to date by the end of March), the potential impact on the year was far less severe than when we locked down in April and May 2020. This is clearly illustrated by the current numbers. As of the end of June the total sales value for the UK golf market was up 72% YTD on 2020. That’s a big jump.

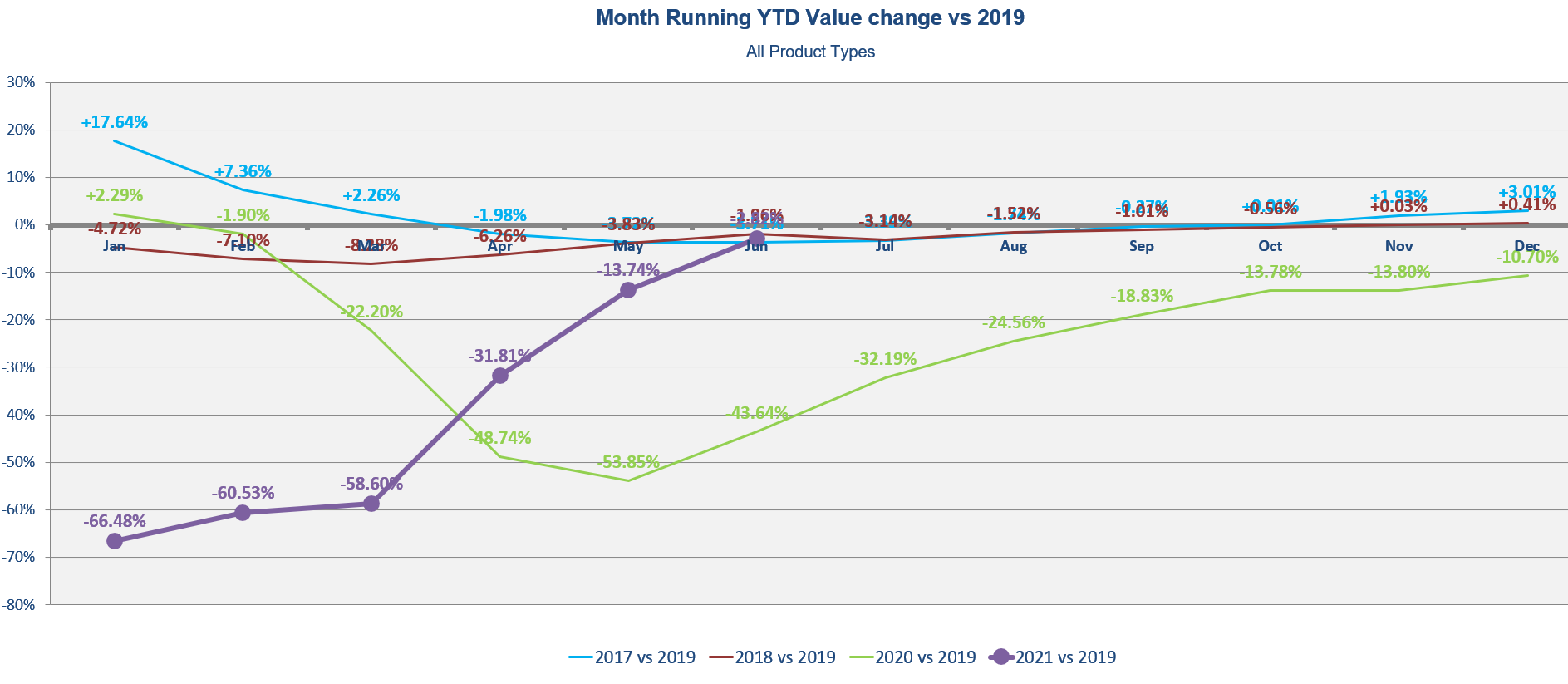

However, we need to remember that percentage changes can be misleading. If we compare both 2020 and 2021 to 2019, things look very different. Compared to 2019, 2021 is still down in total value sales, year to date – but only by 2.8%. In comparison, 2020 was down 42% at the same time. So things are much healthier this year but we are still only getting back to 2019 levels.

What can we learn from this data? Well, there’s lots of talk of a ‘boom’ in golf and, in the short term, there definitely is. However, if we look at it from a long-term perspective, we are currently just level with 2019. So, is there really a ‘boom’ or is this just a return to the status quo?

Looking at the monthly data, we can see that there was pent-up demand following the second lockdown and, since then, the market has been very strong. May and June 2021 were the biggest months that Golf Datatech has ever recorded: with record numbers for a range of categories that we track.

Looking at the sales pattern, I’m confident this is going to lead to a strong year overall, but can we call it a boom? Right now, I think we need a couple more data points to establish the trend but, based on what we see at the moment, we’ll be up on 2020 and I also expect us to be up on 2019. However, the success may not be distributed evenly across all categories. So while some categories are going to have a very strong year, others will probably end up down.

Category Highs and Lows

At this stage, deciding which categories are performing well depends on the context. And, comparisons with 2019, rather than 2020, will enable us to evaluate the real changes in the market. If you look at the year to date changes Vs 2019, there’s a real split in performance.

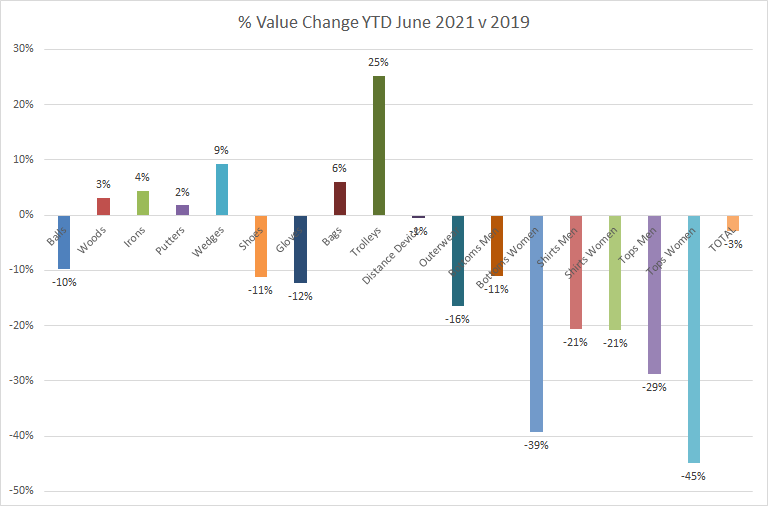

Generally, hardware is doing very well with trolleys the highest performing group at +25%. In fact, all clubs are up as well so hardware brands are having a very strong time. Truth be told, if more production capacity was available, things would be even stronger (I’ll come back to that).

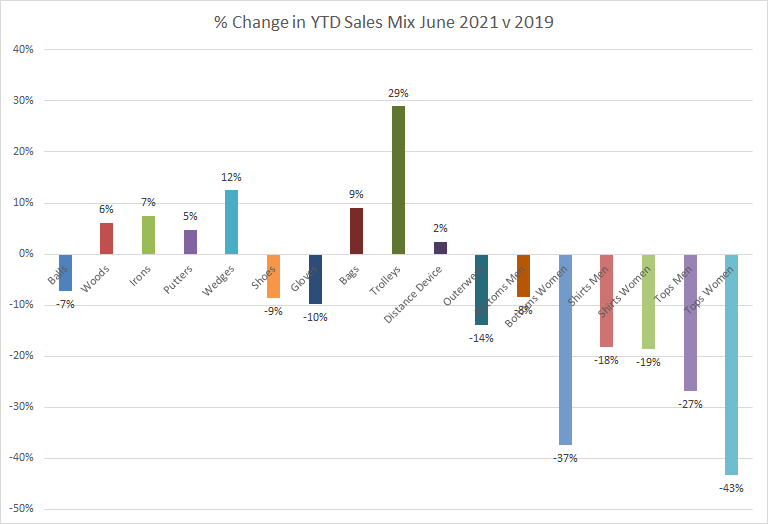

In contrast, on the 2 year comparison, apparel is doing really poorly. All categories are at least 11% down with the worst, ladies tops, down 45% in value. If we look at the impact on the proportional share of sales across categories (the sales mix), we can see there has been a significant swing to hardware, with trolley sales increasing by 29%. This has meant that it has overtaken both shoes and balls in terms of sales importance so far this year.

Does the change in sales mix show us anything?

We should consider why some categories are down at this point in the year. Apparel is a big part of the overall mix and is sold mainly in On-course shops. So, is it On-course that is struggling, or apparel?

If we look at the overall numbers, the issue seems to be based around who, as well as how, the On-course channel is selling apparel. In previous articles, I’ve mentioned that sales decline is down to 3 things:

1 – reduced stock levels and choice

2 – reduced comfort for shoppers in smaller, On-course environments

3 – lack of tourists buying high-value branded merchandise

All of these factors are a result of the pandemic’s restrictions and will probably continue to plague the category for a good while yet. The last point has a significant impact on a subset of golf courses and accounts for a significant amount of value.

In general, Off-course stores are leading the race for sales growth, with much of this supported by online channels. In fact, Off-course is up 8% in value, year to date, versus 2019, whereas On-course is down a similar amount. Part of that difference is accounted for by changes in the sales mix. On-course is hit hardest when apparel drops which is down around 30% versus 2019.

Understanding the current situation

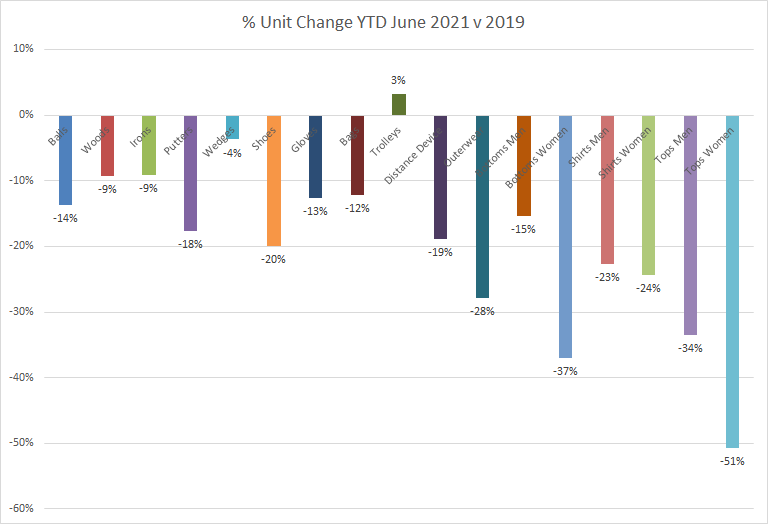

While overall sales value tells us one thing, units can explain other things so it’s worth looking at unit sales and Average Sales Prices (ASP) at this point.

While sales value is up in many categories, this is not the case in units. In fact, only one category is up year to date versus 2019 – trolleys. All other categories are still down.

This might give us a bit more insight as to whether we are, in fact, seeing a boom. Based on units you’d have to say no, but it might be a bit early to tell.

Unit sales tell us how many transactions are going on and there are several reasons for change. We know shops were closed for the first quarter so perhaps we should give them time to catch up. However, there are other factors at play. While the decrease might be the result of a fall in sales, there could also be a leak out of the On and Off-course retail channel to the likes of Amazon and Sports Direct. Unfortunately I don’t have any data for these organisations so I can’t provide numbers here. With Amazon’s growth, they have inevitably done well in golf over the last year or two. What would be interesting is to understand if the growth they have seen has come from traditional golfers switching channels, or from new and returning golfers who don’t have a favourite golf retailer yet. I’m sure there are many new golfers that have been a bit intimidated by the pro shop, or large golf shop, and have preferred to surf reviews and buy online. Moving forward, they represent a great opportunity for the traditional retailer. If speciality golf retailers can engage with these new customers they can offer both price, choice and expert advice. Something that the out-of-channel retailers cannot do.

Looking further into the decline in units, there is more data to explain what might have happened. Looking at ball units, the drop in sales for the first quarter (during lockdown) was over double the difference we are seeing year to date. This is similar for many of the categories. So, while some categories are down, its easy to explain and the reasons may not be so drastic. With much of the season to go, there is a chance for golf retail to catch up (if we stay out of lockdown).

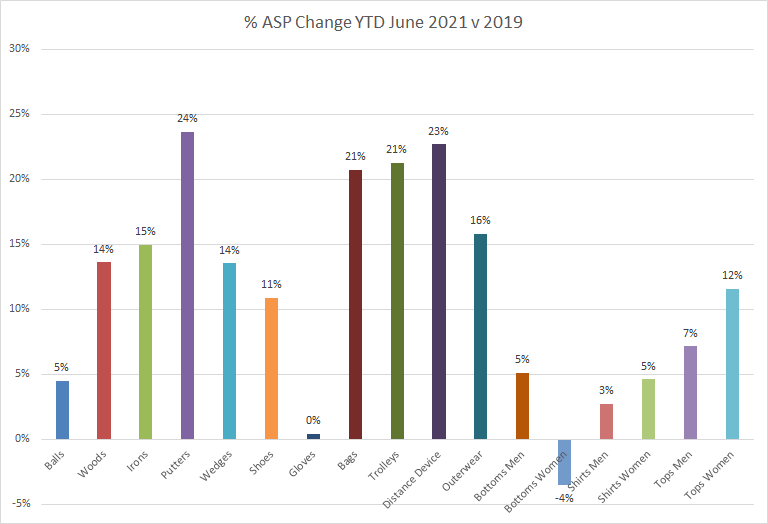

If Units are down and Value is up, then ASP must be up?

Correct. Price increases tell us one of 2 things: that customers are either happy to pay more for the same item than they would have paid in the past, or that they could be choosing to purchase more expensive items. The following chart shows the change in ASP between 2019 and 2021. With the odd exceptions, prices are up a good deal compared to 2 years ago with Putters and Distance devices leading the way, at 23%+ increases.

Any thoughts for the rest of the year?

There are a few things that will determine whether 2021 is a success, or not. First of all, we can only hope to finish the year without another lockdown. I’m writing this on ‘Freedom Day’ and there is a lot of speculation in the media about what this could, or should, look like. Yesterday, there were 50,000 new COVID cases which is the same number as the peak of last winter: the key difference now being that nearly 70% of the adult population has had 2 jabs. This is having a huge impact on the effect that COVID has on its victims. If deaths and hospitalisations remain under control, then hopefully we can get through this spike and everyone can keep golfing. If that’s the case, we should be in good shape to see some solid growth in value, at least.

Another issue that may blunt certain categories’ chances of success is inventory. Unit sales in Irons and Woods have definitely been hampered by short supply this year. Containers that haven’t arrived from China have seriously affected the supply chain. This, along with COVID restrictions at production facilities, has slowed manufacturing. Some brands are now taking up to 6 weeks to build custom fit clubs, and inevitably, reducing sales.

Even with a few hiccups along the way, I still think we are going to be up on 2019, overall. We just have to keep our fingers crossed that we can keep the economy open, keep people safe and golfers on the courses.

Good luck for what is sure to be an interesting few months.