So it’s a another year done and its time to reflect on what’s happened so that we can plan for what’s to come.

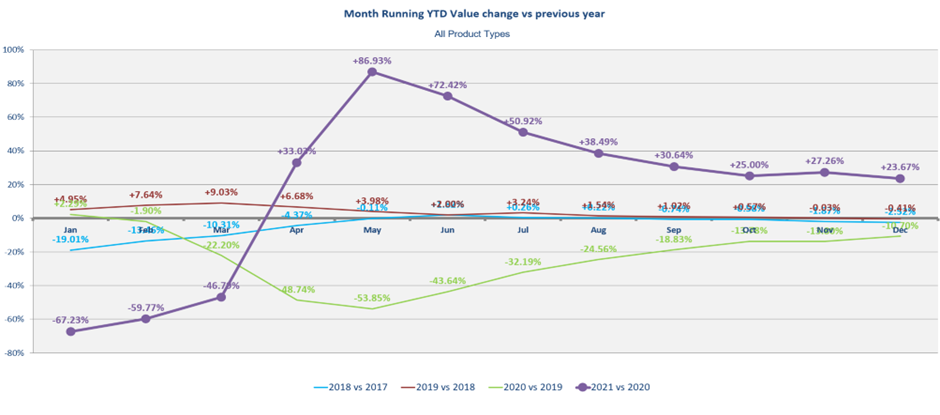

When we started 2021 we had some idea that it wasn’t going to be a normal year. Boy it didn’t disappoint. Lockdowns for the first three months set things back pretty significantly and we started Q2 over 46% down on the previous crazy year. However it’s better to be closed in your quiet months than you busy months. So while Q1 set things back, we were back with a bang in Q2 – in fact by the end of April we were already ahead of 2020 by some 33% in value terms.

Q2 ended up delivering some record numbers – I doubt we will see a Q2 like it for some while. May and June being the biggest months ever recorded by the Golf Datatech UK retail audit.

Q3 started strong with the third largest month recorded. Things started to change in August with sales value dipping under the previous year. In fact the last 5 months of the year would have sat below their 2020 counterparts if November 2020 hadn’t been a lock down.

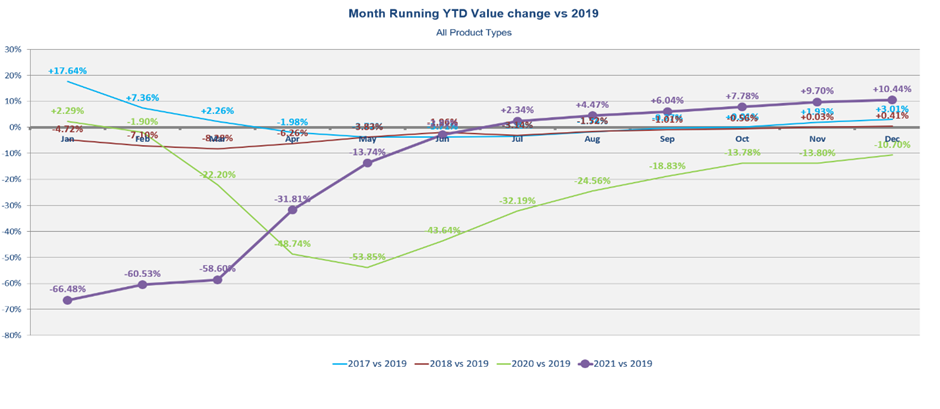

By year end it was a bumper result. Ending up over 23% in value on 2020. More significantly it was up over 10% in value on 2019 – the last normal year. Some brands and retailers would have felt much stronger than that – club retailers were up over 20% on 2019. On the flip side apparel retailers struggled as the category ended down over -11% in value.

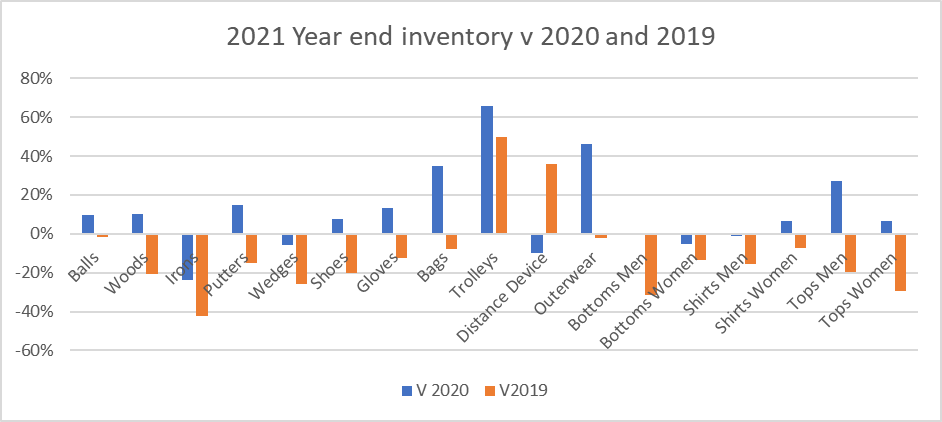

Where is all the stock?

Throughout 2021 inventory continued to be a challenge. Global production and shipping challenges created havoc for purchasing departments around the world. Product didn’t arrive as intended and retailers were short of many items for long periods of time. However things ended up better thatn the previous year. Inventory at the end of 2021 was up in nearly all categories compared to 2020 but it was consistently below 2019 levels. With irons being one of the worst categories with 40% less inventory at retail compared to the end of 2019.

The only categories to be in a positive position were trolleys and distance devices. Both seeing some significant growth.

So how did each of the categories perform?

Breaking things down by category we can see the largest two categories in 2021 were irons, followed by woods. This was similar to the last couple of years, however the gap has closed between the two. If inventory had been more plentiful and custom fit orders fulfilled I think Irons would have enjoyed even more sales. The gap between the two largest categories and the others was fairly consistent with previous years. The third largest category – balls, saw a healthy return on 2020. I believe this is one indicator that there was a slight change in golfers between 2020 and 2021 – with a greater proportion of regular golfers making up the rounds compared to the previous year. Trolleys managed to maintain its place as the fourth largest product category, continuing to keep shoes out of this spot. Shoes continue to decline from their levels of a few years ago. I think this is further indication of consolidation between spiked and spike less sales, as well as some leakage to direct and non-specialist retailers. In the main status quo was maintained with the other categories. Apparel continues to do fair badly in the post covid times.

So how has each category performed?

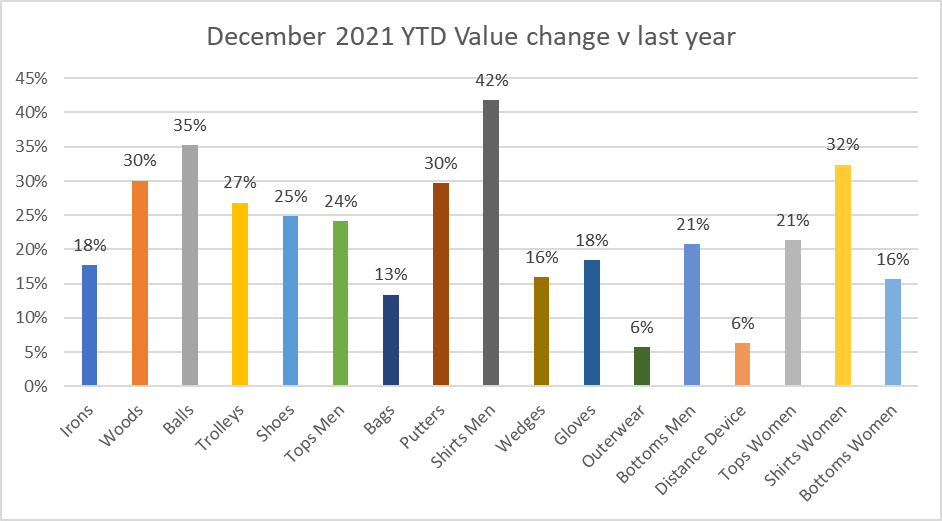

During my previous updates I commented on a continual upward shift in value compared to last year. At year end this trend has continued with all categories up on 2020. Men’s shirts was the largest winner compared to last year. Perhaps no surprise considering how bad apparel was in 2019.

All the main categories saw significant increases with Balls the largest winner in the top 3 – up over 35% on 2020.

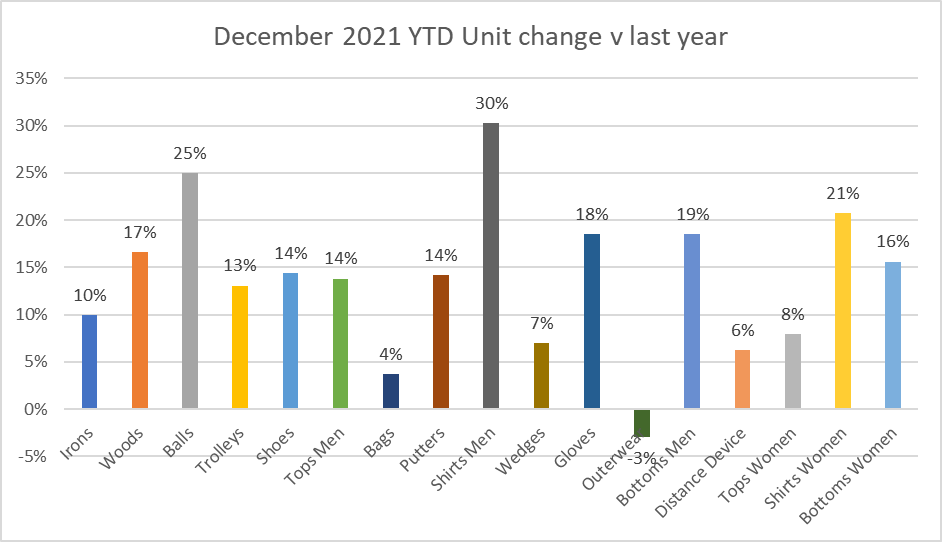

Looking at the composition of the value change is always important. In my previous updates I talked about the gains in ASP and units. By year end all categories except one were up in units on the previous year. Shirts and balls saw the largest gains with more than 30% and 25% respectively.

Categories that really struggled for stock this year included bags, irons and trolleys. Even with the constrained supply these categories still saw significant increases in units versus 2020. However putting a little more context in to the numbers – compared to 2019, it shows a different picture.

While in the main the key categories are up in units – the change is less significant. In addition to this the apparel units – which are traditionally more on course orientated, are still suffering significant losses. Shoes seem to have followed a similar path and probably support the view that customers were less inclined to buy items that needed handling. All in all while we have seen significant value growth, unit changes have not been as significant. Much of this is probably down to constrained supply. It’s interesting to consider how big the unit increases could have been if we had greater stock availability. I am sure irons could have been significantly larger.

And what about Pricing?

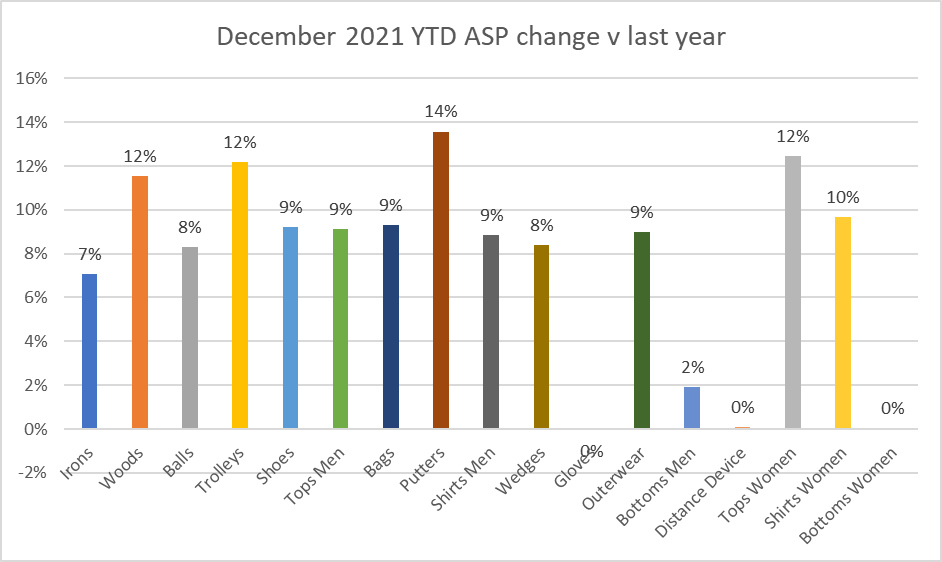

Stepping back to the 2020 comparison, the trend for higher pricing was maintained through the year. All categories either maintained or increased average sales price.

There are a number of reasons for rising ASP. However restricted supply resulting in less discounting was probably the main driver in 2021. Balls in particular didn’t see the usual early promotions, this would have had a positive impact on pricing.

As we move in to 2022 it will be in interesting to see what impact inflation has on pricing and whether improving supply will have a counteracting effect.

Ok so what does this tell us for next year?

Many of the problems are still the same as they were last quarter with fragmented supply and rising costs. However I expect to see the economy starting to have a bigger impact on results especially in H2. The chancellor has written some big cheques over the last two years and at some pint we have to start paying the bills.

I expect the good momentum created in 2021 to carry on in to 2022 for at least the first half of the year (H1). Various things won’t have unwound and assuming we get a good spring people will still be keen to play golf so demand should be pretty strong. From what I hear there is still large amounts of back orders for clubs and they will continue to hit the tills in Q1 and Q2.

Risks still exist in retailers and brands planning. Does everyone have sensible plans for 2022 and order accordingly. We have been discussing the Bull Whip Effect for the last month or two. This could present a real challenge to the industry in 2022 and through to 2023. For those unfamiliar with this concept here is a quick summary. The idea is that a small reaction from consumers can have an large effect on manufacturers. Like a bull whip, you flick the wrist a few inches but the whip end moves many feet. When there is a spike in demand retailers who have sold out or lost sales due to low stock place larger orders for stock. They don’t want to miss out next time. As a result wholesalers and distributor do the same but add a bit more just in case. This works down the supply chain to manufactures who scale up production to make sure they satisfy all the demand – plus a bit more. Obviously this all takes time and when often happens is by the time the stock is made and heading to the retailers – demand has cooled. A new problem appears – there is too much stock heading to retail. In addition to this the incoming stock is not what the customers now want. Its pretty easy to see that a scenario like this could occur in the golf trade if retailers and brands eye further growth or expansion. I have a feeling it might be hard for some to curtail there orders but it might be the sensible thing. We really don’t want to return to the bad old days where clearance was a major issue for the industry.

Planning sensibly for next year is key. One of the key questions is what does the new normal look like? Unfortunately we don’t have a crystal ball so we are going to have to look at the numbers to make an estimation. Looking at the trend for H2 2021 the numbers would suggest some consistent elevation over 2019. Looking at general sales values, the shift from 2019 was pretty consistent over the last 5 or 6 months. With the second half of 2021 cutting a constant path between 2019 and 2020. I think this bodes well for 2022. So if I was doing my planning I would start back with my 2019 numbers. If I was optimistic and looked at the H2 trend I would hope that general spend should be higher than 2019 somewhere between 5 and 10%. How that spend is made up could be very different to 2020 and 2021 and that might be where things become tricky. I think clubs could remain high, there is lots of good kit coming out and there is still pent up demand. Clothing might see a return as it has been hit hard over the last period. You would also expect travel to open up and that would increase soft goods sales. However on the flip side, if travel opens up we might see lots of Brits heading abroad and spending their hard earned cash on holidays and experiences instead of goods.

One other thing to consider going forward is the is where consumers spend their money. Looking at the market overall there has been some shifts in consumer behaviour in 2022 and 2021. A lot of sales went online in both traditional and non-traditional golfing outlets. Some of the new golfers in particular shopped out of the speciality channel. Amazon would have done very well in 2020 and 2021 however this trend may reverse. Towards the end of the year there was a sense that customers were starting to turn their back on online in preference for bricks and mortar. They just wanted to get out of the house and see and touch some things!

Whatever happens in 2022 with the economy or Covid there is one thing to remember. Golf is very resilient industry and avid golfers play golf whatever happens. Hopefully that will remain the case in 2022 and the industry has solid year. You can be sure that we will keep counting the sales and inventory and providing insight to help brands and retailers make smarter decisions.