I started writing this just before Christmas, before being distracted by mince pies and turkey. So, let’s backtrack and take a brief look at how the UK Golf Market faired in November.

As before, we are using comparisons to a previous lockdown and November looks pretty awesome.

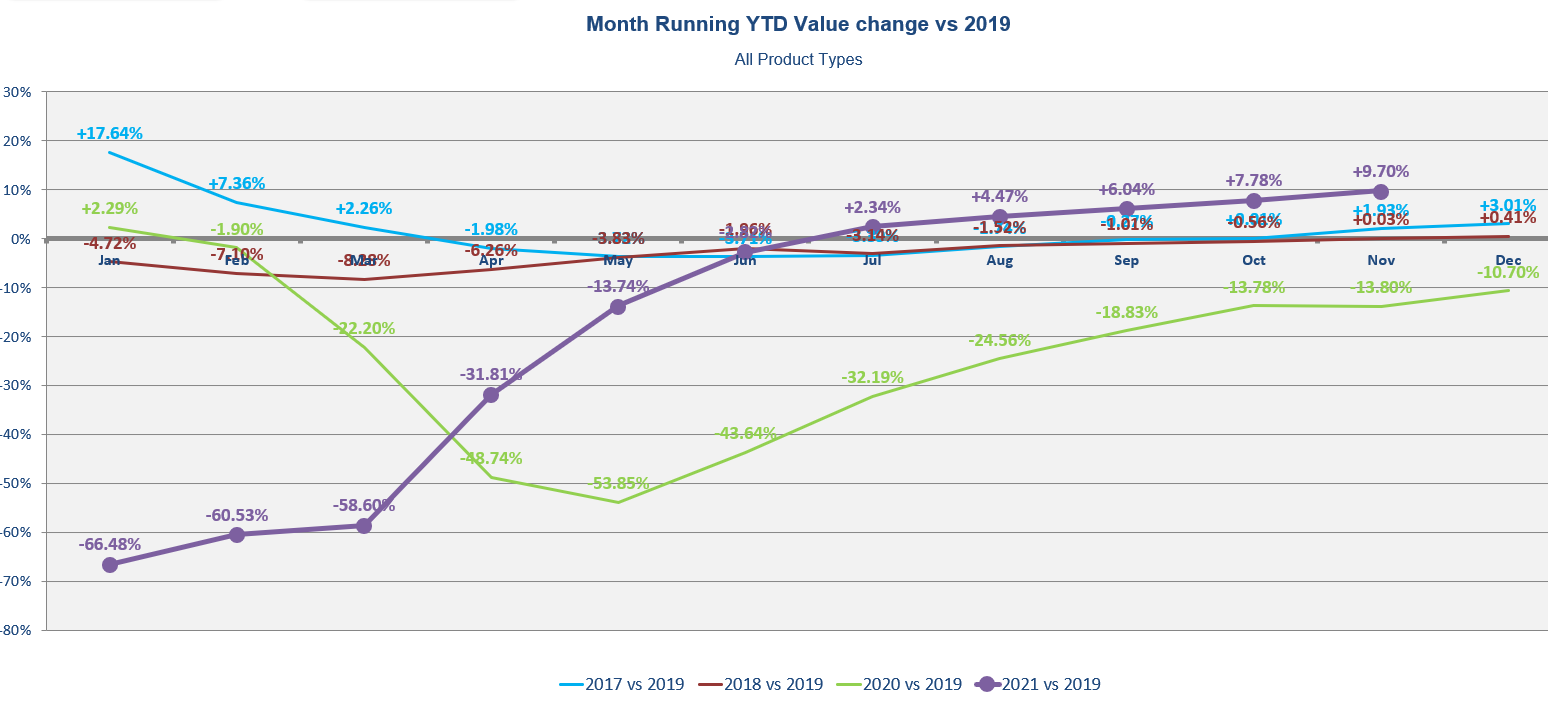

According to the Golf Datatech UK retail audit, sales values through the golf speciality channel were up over 58.3% on 2020, and a very impressive 35.9% up on 2019. Now, that is real growth. That puts us at a year to date +27.3% up on 2020 and +9.7% up on 2019. In fact, taking out slow apparel sales, the main hardware and durable categories are up over 18% on 2019.

Best and Worst Categories

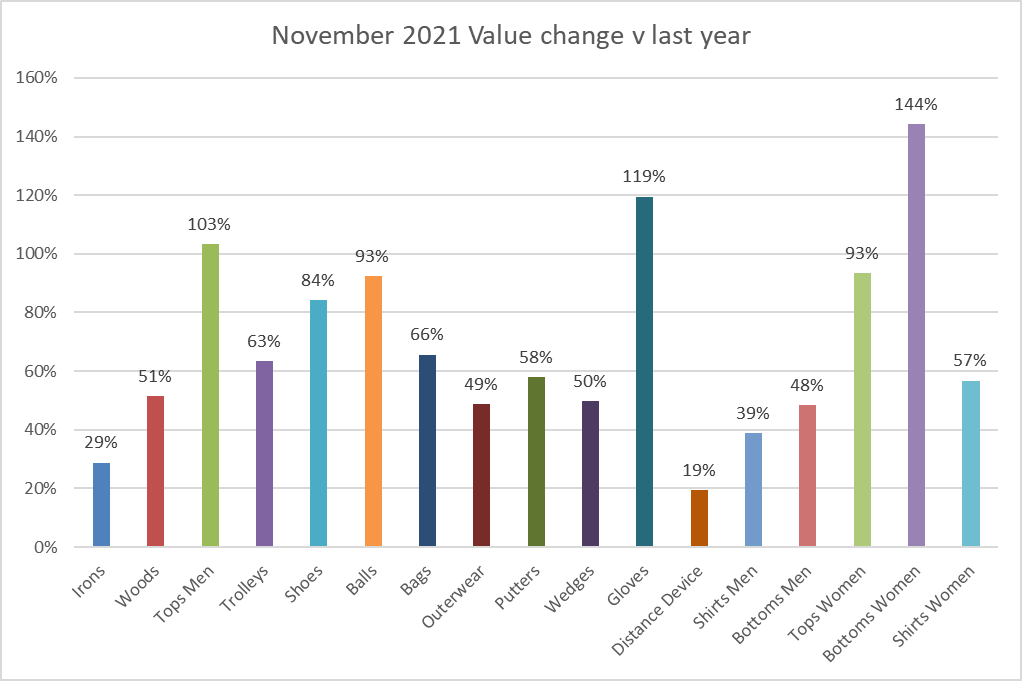

Looking at sales change v 2020, gloves, ladies bottoms and men’s tops were the best performing categories – All seeing growth of over +100% on 2021.

Against 2019, the best performers in November were putters and wedges, with both categories over +50% bigger than 2019.

Year to date v 2019, the story is a little different. Trolleys saw the biggest change – up +24.5% on 2019. While women’s apparel – bottoms and tops – were the poorest performers. More than -29% down.

Are the Changes in Units or ASP’s?

In the 3 largest categories, woods, irons and balls, all units are up v 2019. Overall, 6 categories saw positive growth in units while 11 saw a decline. By and large, it’s the apparel categories that faired much worse.

In ASP, there is universal growth over both 2019 and 2020, with the odd exception of ladies’ bottoms. The largest price rises came in putters – up +24.4% v 2019, and trolleys – up +22.5%. The average trolley spend rose from £341 to £412. That’s a big jump in 2 years.

Nine out of 17 categories saw double digit average price increases in 2 years.

On and Off-Course Comparisons

Both channels actually did very well. Off-course (with its greater online presence) is up over +40% in November compared to 2019. However, on-course also saw solid growth and was up +30% for the same period.

Inventory Challenges

As you might well expect, inventory is a bit of a challenge. While units are up generally v 2020, they are down in nearly all categories v 2019. The biggest drops came from irons, men’s’ bottoms and women’s’ tops. All down circa -30% on 2 years ago.

Despite this, there are categories that have seen big increases including trolleys, which was up over +30% and distance devices, up over +68%.

What Next?

Well the year end is here and we will be compiling the data for December over the next 2 weeks. Up to the end of November, the market is up, year to date over +27% in value versus 2020. No surprise there. What’s more important is that we are nearly +10% up on 2019, which makes 2021 the best year ever so far.

Expectations for December are that it wasn’t a great month with most high street retailers seeing a drop over 2020. No doubt, last year, there was some pent up demand after the lockdown. So, while the gains on 2020 will be trimmed, we are still likely to be up against 2019.

The next question is whether the momentum can run well in to 2022. Will new golfers remain and keep spending? Will travel help golf destinations to sell more clothing, or will it send golfers elsewhere to spend their money?

Lots of questions which will become apparent as the data is revealed.

Happy New Year!