I am needing to get by Blog back up to date so I thought I should backfill some missing articles. So better late than never – here is a round up of where golf retail got to at the end of 2022.

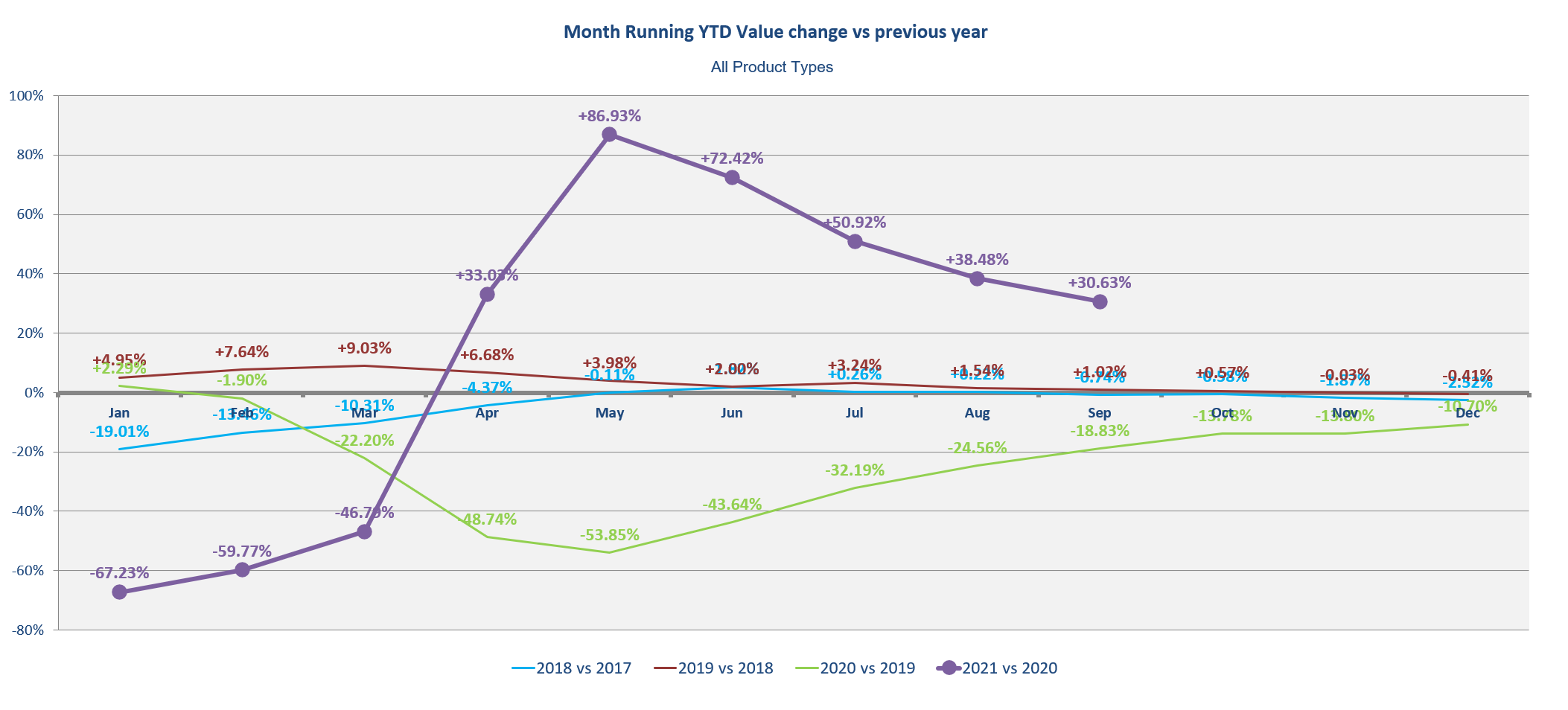

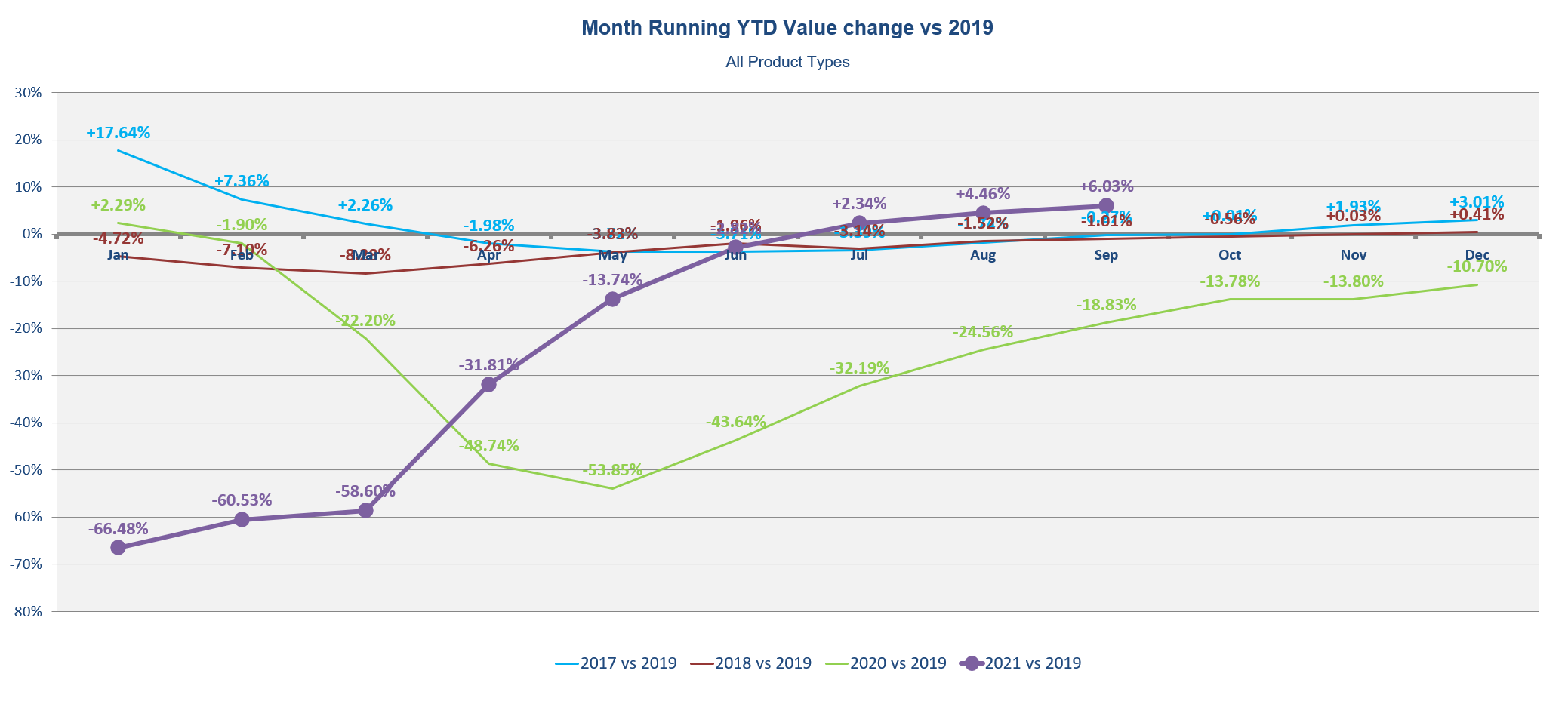

After two years of chaos, 2022 has ended up being relatively straight forward for the industry. Indeed it was pretty similar to 2019 – just a bit bigger. For most people in the industry we should take some comfort from this. With all the apparent changes with participation etc, the retail market returned to relatively predictable norms.

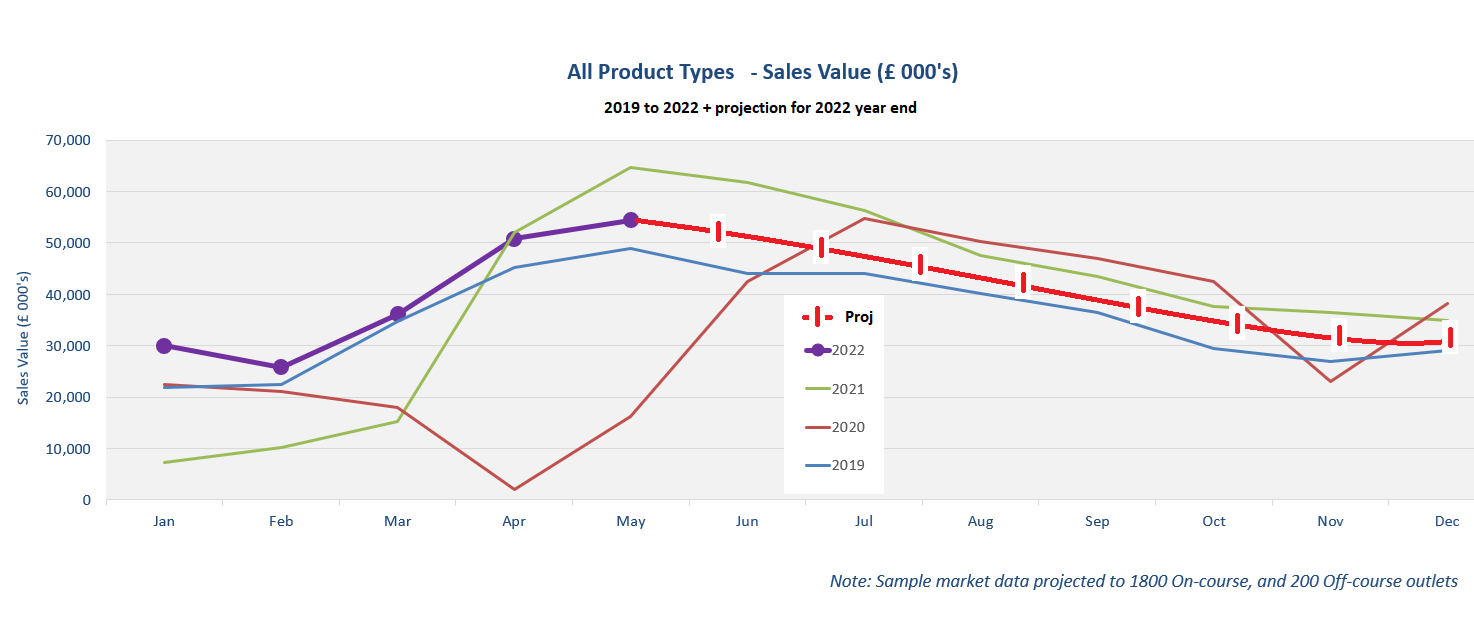

I am often asked to make predictions on the year and I was concerned I might have shoot myself in the foot in May. I made the following forecast for the remainder of 2022.

By year end I was pretty relieved to see that things turned out pretty much as predicted. There was a slight bump at the end but otherwise the stats had been relatively predictable.

Actual sales levels up to year end.

This isn’t me trying to be a know it all but it is supposed to illustrate that with decent data and some reasonable assumptions, we can have a good guess at what might happen from a fair way out. This is good for all our businesses.

There are a few things to consider

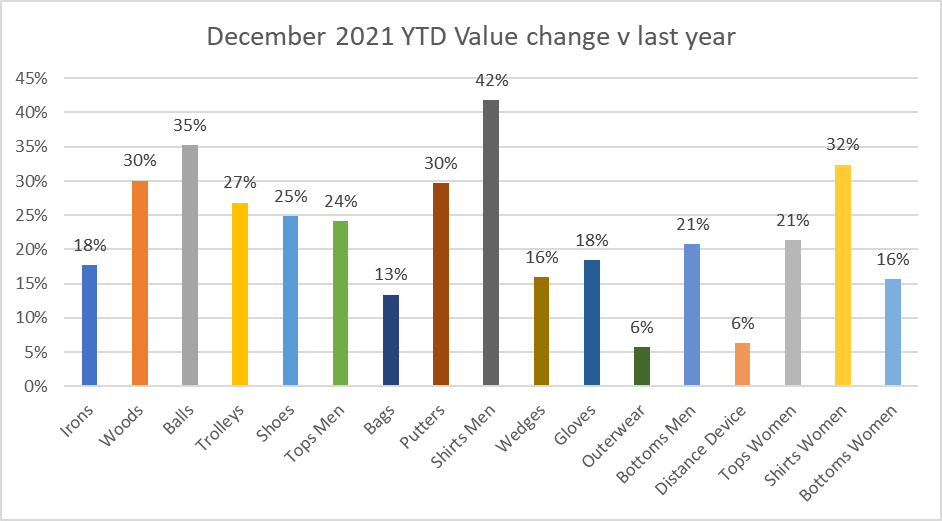

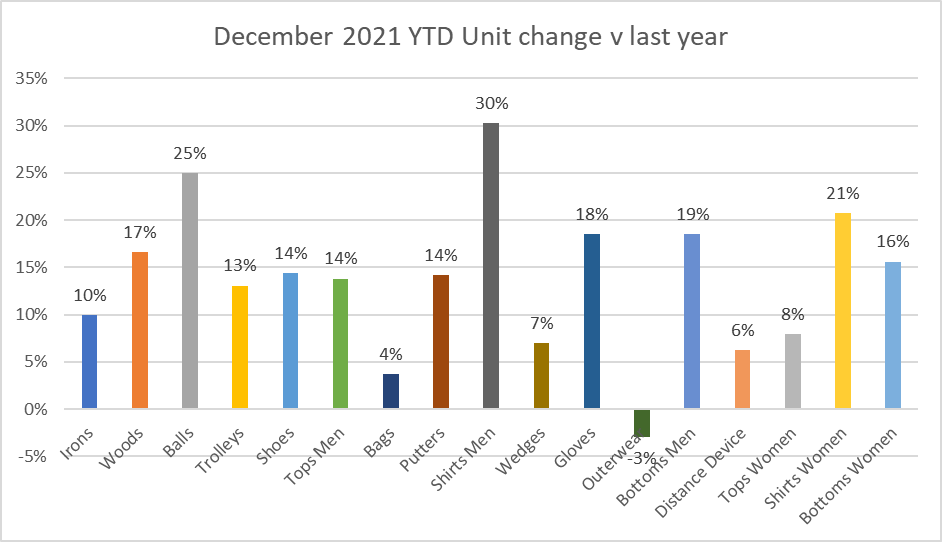

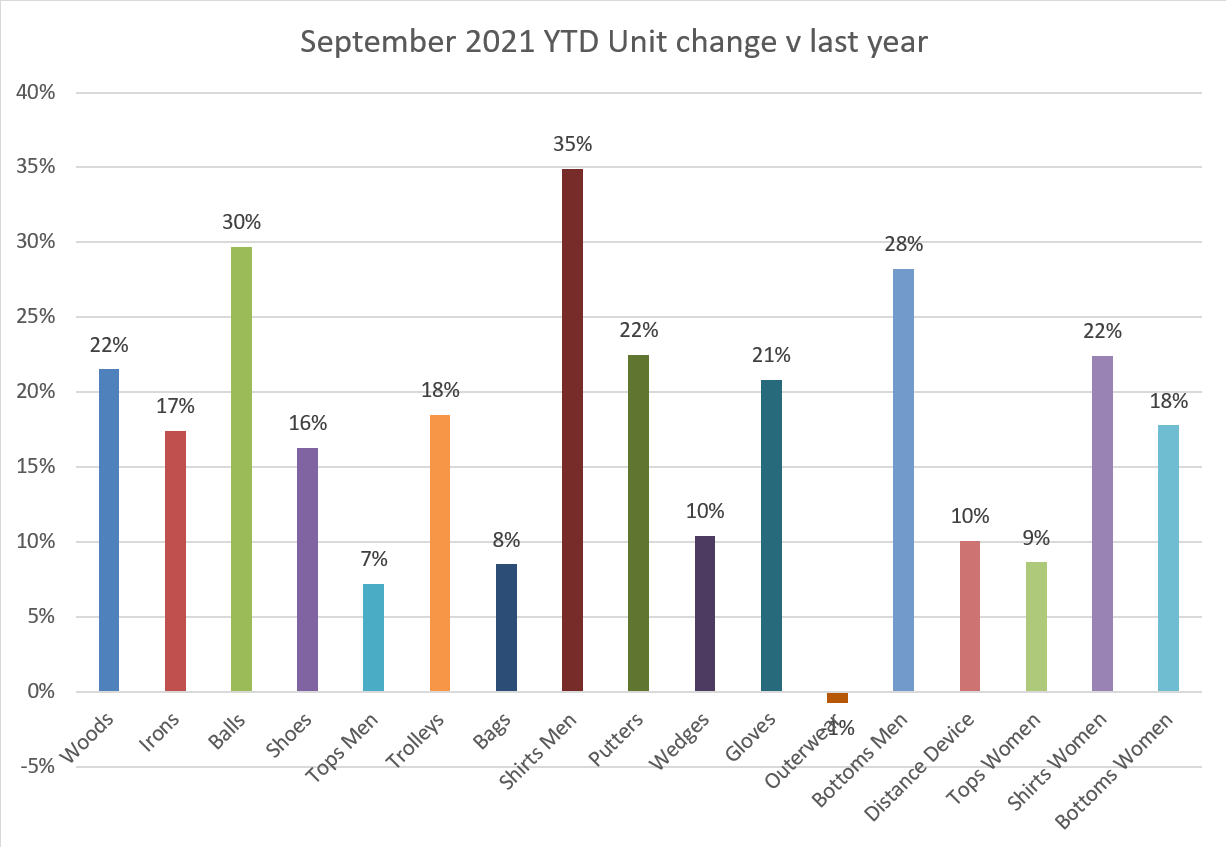

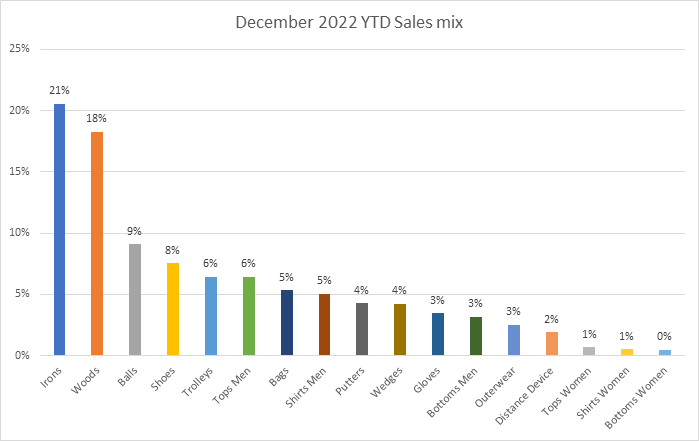

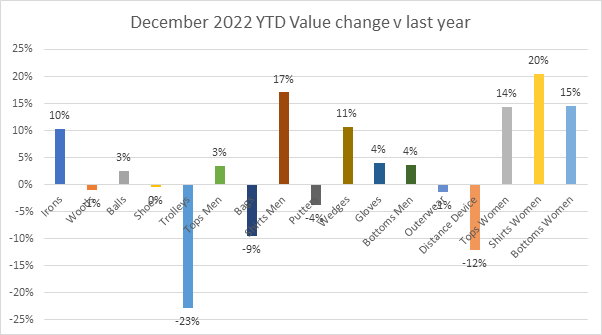

So overall spend was pretty solid up nearly 1% on 2022 and over 13% on 2019. However the mix of spend was quite different. While Irons topped the table with over 21% of sales the biggest looser was Trolleys. Having been in a position to compete for the number 3 spot in the last couple of years. Trolleys dropped over 23% compared to 2021, making it the fifth largest product category – overtaken by Shoes. Outside of the big two Woods and Irons, sales were more evenly distributed amongst the other 15 categories tracked by Golf Datatech.

Generally, apparel had another weak year. While sales had increased on the prior year and now matched 2019. Sales of soft goods are relatively poor compared to Clubs that have seen an increase more than 25% since 2019. Much of this has been discussed before and there are various well-established reasons for the decline. What I would say is that I expect Apparel to be one of the big winners in 2023.

Looking overall there wasn’t any real consistency in value change. Some high value categories were up, others down. Overall consumables were up and generally so was apparel – but it must be remembered that this was off a low base. Bags saw a similar fate to Trolleys with a nearly 10% decline. While Distance devices were also a significant looser. Wedges followed Irons and grew double digits but Putters dropped the most of the club categories.

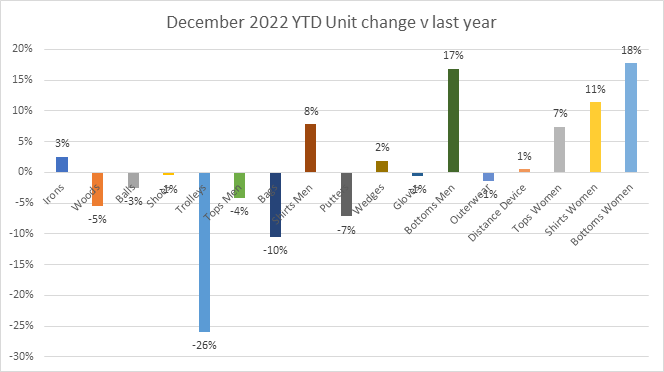

Stepping away form value and looking at units. The trends were similar, Irons and Wedges grew. Woods and Putters didn’t. Trolleys and bags plummeted and apparel mainly went the same direction as value. The main exception was Distance devices. Having seen a big value drop – units were actually up.

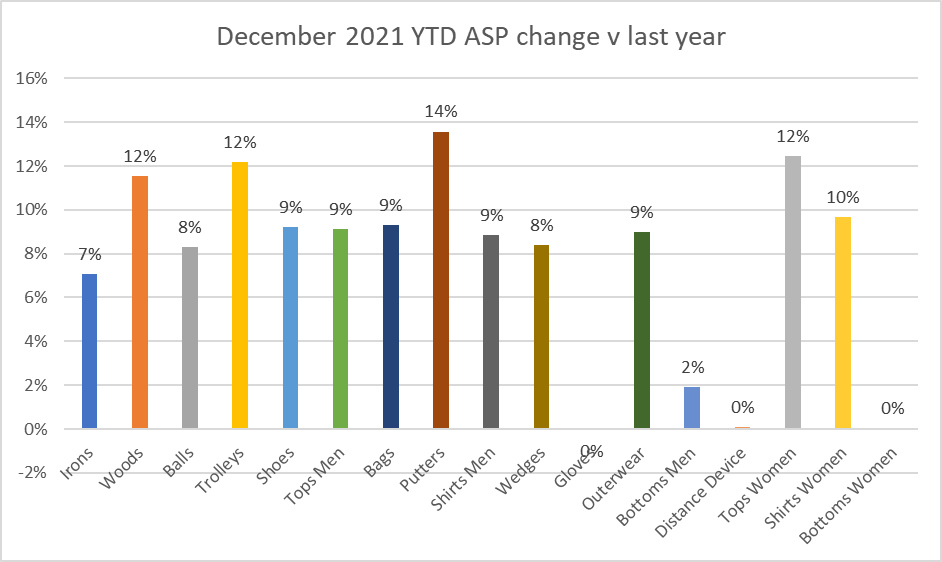

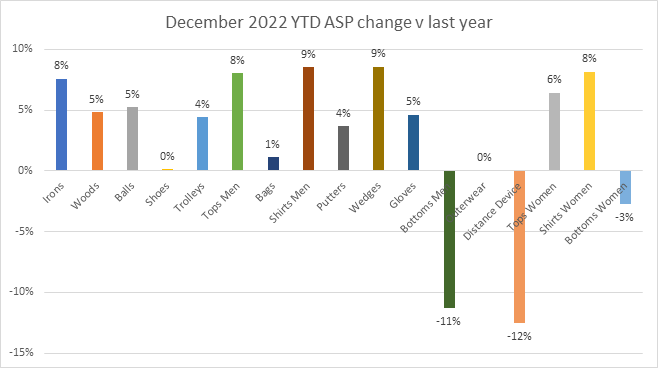

Looking at ASP tells the rest of the story. Distance devices saw the largest drop in ASP for 2022 down over 12% and bringing the whole category in to decline. Introduction of lower priced products seem to have brought down the overall spend in this category.

Interestingly the same issue seems to have effected Bottoms that saw a decline in ASP, where as all other categories appear to have become more expensive.

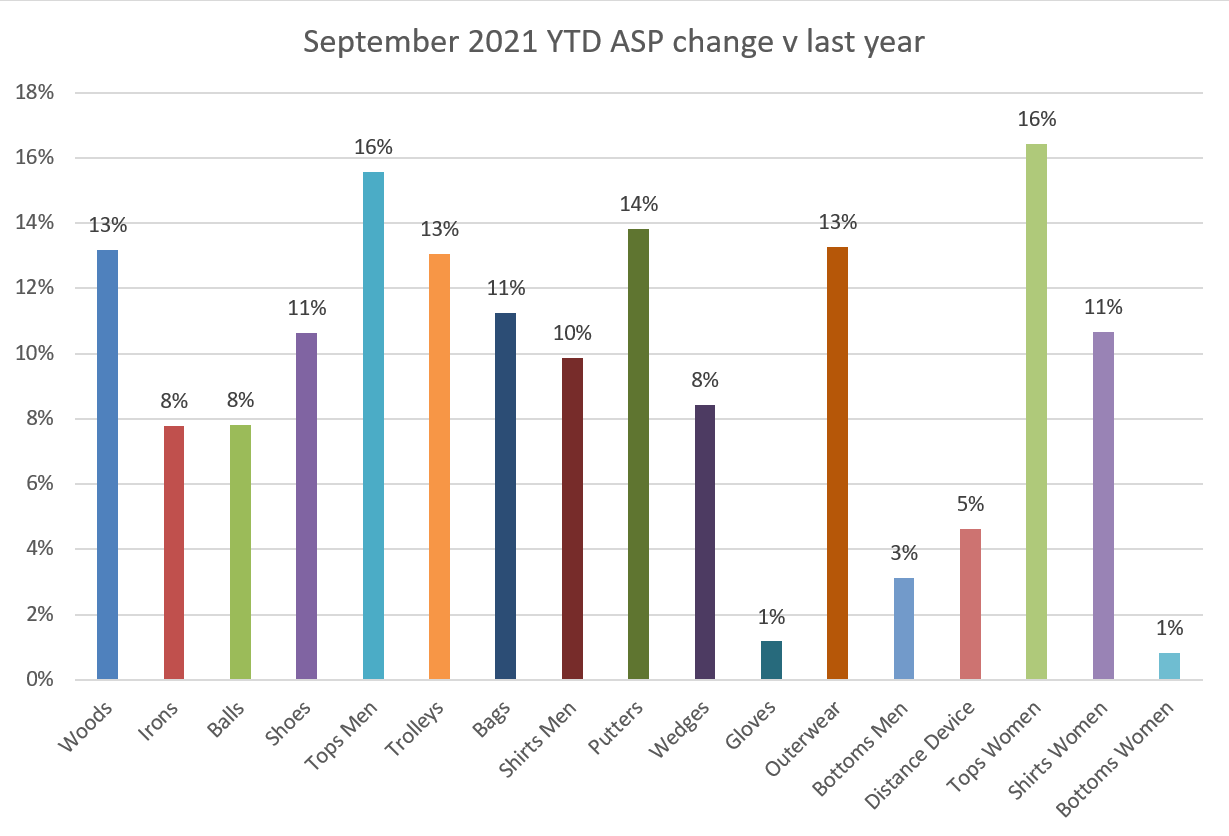

So overall ASP was up across the majority of categories. With Mens shirts and wedges leading the way at a 9% increase.

Are prices too high?

Some of the categories are reaching seemingly elevated levels. There has been quite a lot of concern about the current price of drivers. With a number of the big brands bringing out their new clubs around £500-£530. Some think this is too much.

I have a couple of thoughts on this. Firstly its interesting to note that if you inflate the historical prices of the top selling drivers from 2000 or 2015 they are actually very close to todays prices. If you use some of the online inflation calculators, £249 (the ASP of the top Callaway driver of the day) from 2000 is the equivalent to £536 today. So in real terms prices have not increased out of line with everything else. Stuff is just more expensive, however over the same period wages have also increased. According to Statista “Median annual earnings for full time employees in the UK” went up from £18848 in 2000 to £33000 in 2022. So as a proportion of annual income the new driver prices have increased by 20%. However this is only of the median earnings, if you were to look at the average earnings of golfers – the details might be very different, which takes me on to me second point.

We need to remember that Golf is a luxury activity and is only played by 7 to 8% of the population. You don’t have to play Golf and not everyone can afford to play golf. No one is forcing anyone to buy the newest items. People can choose where they spend their money. However if you want to play with the newest and shiniest equipment, there is a cost and for some items this is high. Many commentators have noted that demand for luxury and high value items has been maintained through the current economic woes. Proving that those with money are still happy to spend it. For some that will include golf clubs and should give us some confidence that people will continue to spend money on things they WANT. The only consideration is – what proportion of the consumers fall in to this bracket – has this changed. If so will this affect volume sales?

The third point is that while the newest equipment from the biggest brands is demanding high prices, there are plenty of alternative choices available at lower price points. Not everyone can afford a Ferrari – most will buy a Ford or BMW instead. There are several second tier brands offering excellent equipment at lower costs – indeed this may present an opportunity for them as consumers start to consider different options. We should not forget that there is also a lot of second hand equipment easily available through various retailers. This also provides options for consumers to resell their old equipment to fund their new equipment. All these options provide consumers with choice.

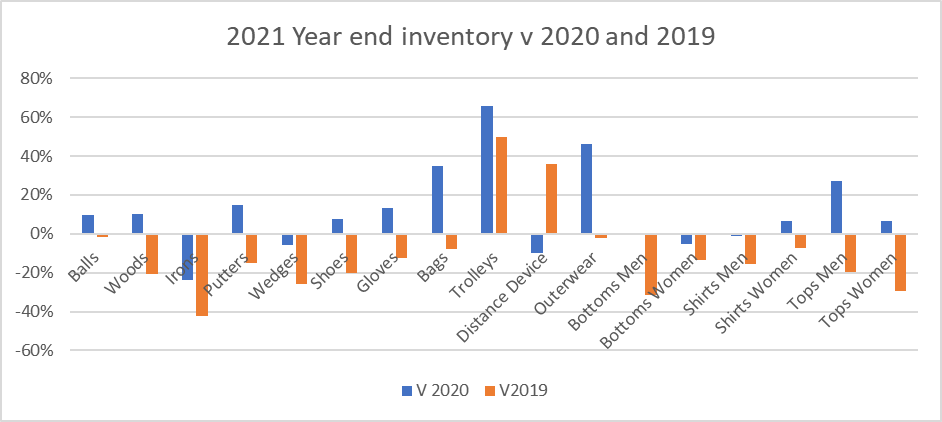

So sales have been good – are we left with much stock?

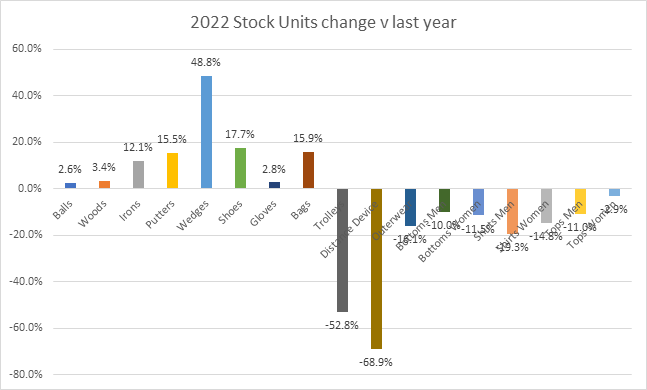

Well compared to 2021 – we have more hardware and consumables but a lot less apparel. This has been a pretty consistent theme in 2022. Supply chains caught up in some categories and over shot in hard goods. As you can see below Wedges have had the biggest increase in stock. While distance devices seem to have disappeared from many shops.

Challenges remained in soft goods for the first half of the year which meant the industry was short in a number of categories. This persisted through the year. Finally trolley woes resulted in a big destock at retail. Both soft goods and trolleys suffered on the sales front so it will be interesting to consider if the stock shortages were a cause or affect?

Final thoughts

Moving in to 2023 (I know we are already a couple of months in) its worth reflecting on last year to see what we can glean for this year – after all at this point there is still over 90% of the year to go.

In normal years total spend has been pretty consistent year on year, traditionally with single figure changes overall. Even during the pandemic things didn’t shift seismically on an annual basis. What did change is the position of the different channels, with online growing and then declining. In the US its interesting to see that the online channel has shrunk back to pre pandemic shares of sales. Its larger than it was before the pandemic but as a share of the total sales it is actually smaller. In the UK we have seen a move back to the on course in 2022. The off course and online are bigger than they were but can then pull back some of the customers they have lost in the last year or will the on course continue to grow?

Another factor to watch this year is the effect of “revenge travel” as consumers look to escape the chains of the pandemic and get out to see the world. For those in the UK that travel abroad it might be money out of the golf budget – which could hit sales. This might have a greater impact on the casual golfer than the avid. Conversely there will be plenty of visitors that choose to come to the UK and spend their dollars here. As the £ is relatively week it will be cheap for many visitors, so their spend could be strong.

My general expectation for 2023 is that spend will be similar to 2022. If the weather is good then it might be up a bit. If the economic woes way on the general public it might be a bit down. The spend profile is likely to be a bit different this year so changes within categories could be more significant. I except irons to soften and for woods to do better. Putters might also pick up from last year. I expect apparel to do better this year with improved inventory and increased visitors.