There has been a lot of challenges thrown at the golf industry recently. COVID, weather and supply chain are all trying to make everyone’s life a bit more complicated – or interesting if you have a masochistic streak! With all the changes come lots of moving numbers and, with that in mind, here is an update for July.

Another big month

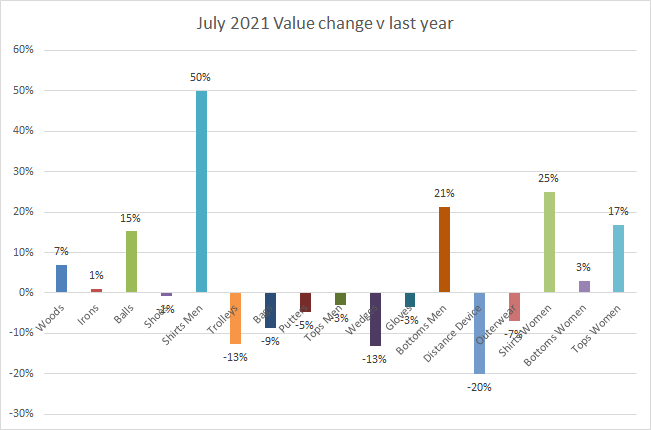

July 2021 was the 3rd biggest month we have ever recorded. It was bigger than July 2020, which was the record month until earlier this year. In total value July 2021 was 2.9% bigger than 2020 and was 27.8% bigger than July 2019. Year to date we are now 50.9% up on 2020 and for the first time up on 2019 by 2.3%.

All categories weren’t equal. Irons and woods saw some growth but this time it was the apparel categories and balls that saw the largest changes. Men’s shirts jumped 50% on last year finally showing some positivity for the embattled apparel categories.

A number of categories were down, including trolleys and distance devices. These have both been hot categories and shown strong in previous months. It’s now a question of whether the demand for these products has been satisfied, or is stock effecting sales? Certainly for trolleys, stock might be an issue. While the off course has increased stock holding on the last 2 years, the on course retailers seem to have a lot less – nearly 50% down in units on 2019.

Are Inventories generally down?

The stock numbers are a little misleading. Initially, things look good, with most categories up on last year. However if we take a longer view, we can see that all but balls and distance devices are down on 2019 and most by a lot. Irons are down 29% on two years ago. However, these figures only tell us part of the story.

Stocking in the key hardware categories is very different on and off course. Wood and Iron inventories are down double digits on course – irons down a massive 53% on 2019. This is not the case off course with both categories being in a stronger position than 2019. Off course retailers seem to have taken a chance and stocked up in key areas to try and ride the wave of demand.

Where is the market heading?

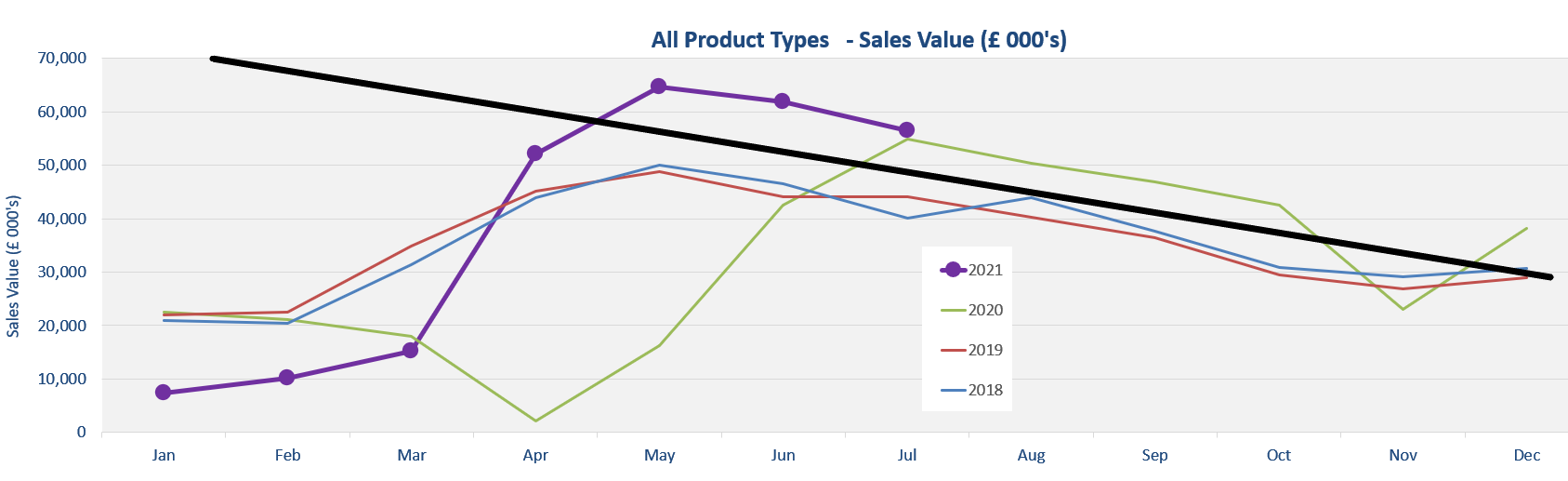

Looking at the monthly sales graphs we have some clues. If you look at the graph below – sales value by month for the last 4 years – you can see that, once the market hits a peak, it typically trends down in a fairly consistent manner.

The last 3 years all run in a parallel direction to the black trend line. On that basis, we would hope that 2021 will work in the same vein. It has done so for the last 3 months. The only thing that might create a few bumps is lack of stock and the odd bit of extreme weather.

All things considered though, I expect the market to trend in a similar way to last year – perhaps a few percentage points down. However, the mix of product might be different, with apparel improving and clubs softening. Overall that should put us somewhere near 15% up on 2020 and 4% up on 2019 although that will feel quite different if you are club brand or an apparel brand. Clubs will be up double digits while apparel will be down.