Right now, golf retailers are slap bang in the middle of the season. It’s one of the busiest times of year for pro shops, and all too easy to lose track of how the market, and your business, is performing. The April retail statistics were recently released, so let’s stand back to look at the picture so far, .

2019: the story so far

By all accounts, it’s been a good start for both golf retail, and golf, in general. Both Winter and Spring were very kind, (no snow), allowing lots of play in relatively warm, and dry, conditions.

People out on the course have been spending money, while Tour Professionals have been generating a good deal of media interest. Tiger Woods winning his first Major in 11 years was, perhaps, one of the greatest comeback stories ever. Everyone seemed to be talking about it: even my football-obsessed builder!

Rory McIlroy returned to his winning-ways: taking the unofficial 5th Major at the Players Championship. While Brooks Koepka retained his PGA Championship title, in dominant style, with an imperious win. All great stories from interesting players, capturing a lot of screen time and news updates.

The Numbers to Know

According to Golf Datatech‘s retail audit, the first 4 months were up in value across the core categories:

- January up 4%,

- February up 10%

- March up 10%

- April up 2%

This is a really strong start that left us up nearly 5%, year to date, at the end of April. Looking at slightly longer trends, this was just under 1% higher than the same time of year in 2017, 16% up on 2016, and a huge 23% up on 2015. Anyone who thinks the market isn’t moving forward is mistaken.

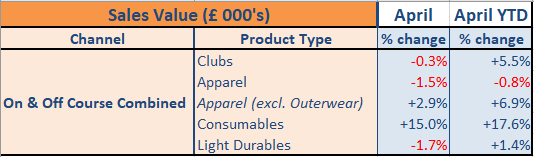

The first 4 months of the year account for around 28% of total sales. During the largest, April, most categories had a healthy increases during the month, in year to date values.

Balls had the largest jump: up nearly 20% in April.

Of the core 15 categories, 8 were up and 7 were down. However drops were relatively small. Apparel saw a strong start, with only Outerwear dragging the numbers down. Unsurprisingly, all the good weather has meant that this was the worst-performing category.

“Anyone who thinks the market isn’t moving forward is mistaken”.

Looking at the numbers, Clubs seem to have had a little bit of a dip in April. This was off the back of a very strong start to 2019, and in comparison to a very big April 2018. Overall Clubs are up 5.5% in value, year to date.

Its worth remembering that, last year, April and May were really odd months. April 2018 was the 3rd largest month we had ever recorded, with May the biggest. We put this down to lots of pent up spending following a bad winter, so year on year comparisons are going to be a challenge for these 2 months. More on that in the May update next month.

Was there an increase in units?

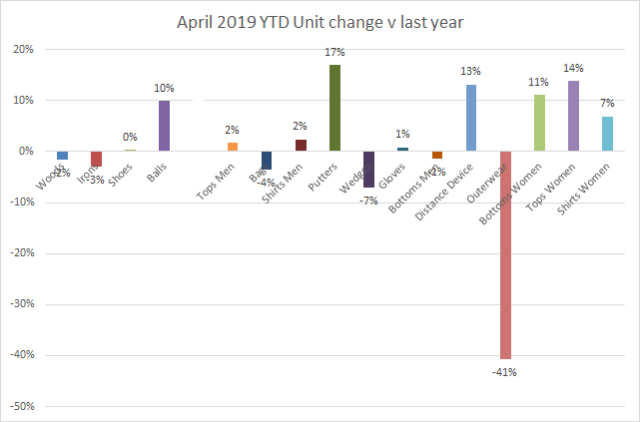

I’m glad to say that year to date, units are up in 9, of the 15, core categories. Three of the 4 Club categories have seen a little softening: just down a couple of percent. Putters continue to surge forward, with more than a 16% increase. Ladies Clothing also had a strong start. Only Outerwear really took a tanking!

What have people spent their money on?

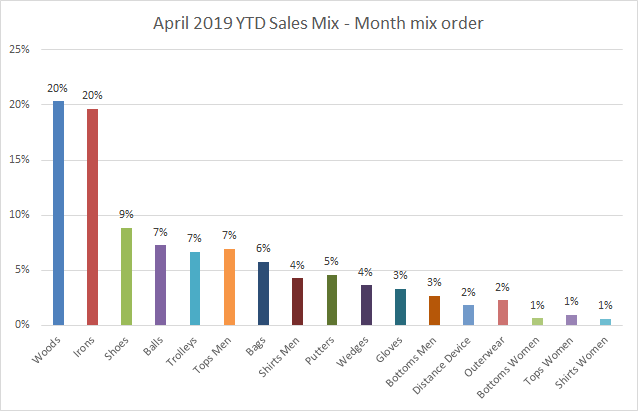

There was a change to the mix this year with Woods becoming the biggest category: taking over from Irons, year to date. Shoes and Balls were in 3rd and 4th spot, indicating healthy participation numbers.

Anything else interesting to note?

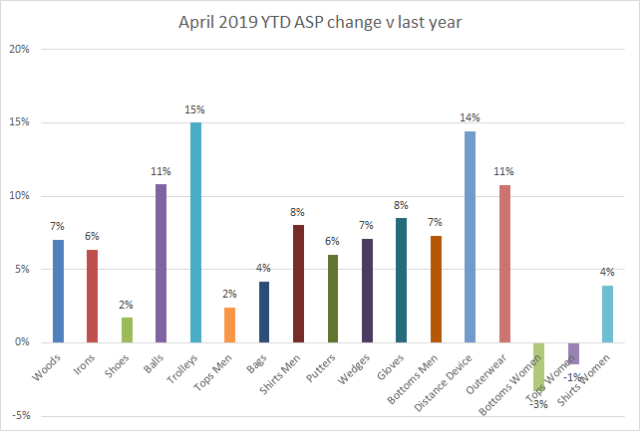

One thing people are talking about is Average Sales Price (ASP) and, as you can see from the graph below, ASP’s are up again this year. There’s been a relentless march of price increases over the last few years, and this year, all categories, apart from Ladies Tops and Bottoms, are up year to date.

While prices aren’t arbitrarily going up on the same products, the new products coming to market are driving prices higher. I do wonder how much the consumer is willing to pay on some categories.

“In 2015, 23% of Drivers sales were in the ‘£300 and over’ category. In April 2019, this price band accounted for 78%.”

If you look at this year’s biggest category, ASP on Woods has increased 48% over 4 years. Driver price points have increased considerably. In 2015, 23% of Drivers sales were in the ‘£300 and over’ category. In April 2019, this price band accounted for 78%.

While price isn’t the only factor changing buying behaviour, (lots to talk about custom fit, launch monitors and £/Yd), it’s interesting that over the same period, unit sales have dropped by 19%.

What about next month?

Well to be honest, I pretty much know what’s happened. Expectations were for a good month, but not, maybe, as healthy as last year. The figures seem to support that. Full update for May will be published next week.

As always, I’m happy to help and answer any questions you might have on the market data, so do ping any thoughts, or queries, across to me.

For more information about Golf Datatech’s retail audit data, covering all the key golf categories in the US, UK, Sweden, Germany and France, contact Phil at pbarnard@golfdatatech.com