And the sun kept on shining!!

It wasn’t very long ago that I was all doom and gloom. Poor weather at the start of the season was having an impact on sales, and the market numbers were down. But since April, I have been repeating the same old story – the sun is out and people are playing golf and spending money.

Its incredible how dry it has been. You only had to look at the Carnoustie during The Open, to see how much so..

.. with the few lush greens a stark contrast to the scorched brown rough and fairway. A pretty setting, for what ended up being, a fantastic Open.

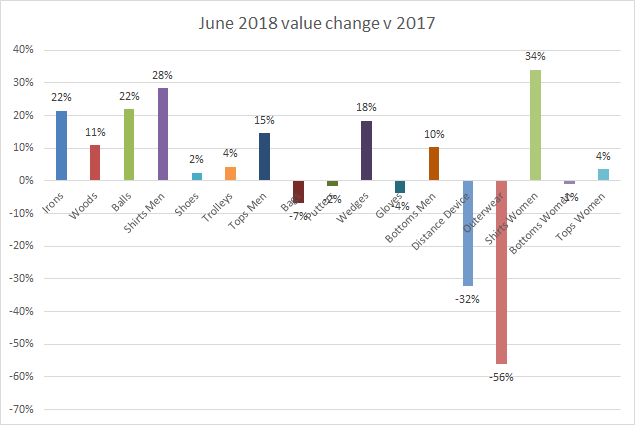

June Market Numbers

Another pretty picture was June’s retail market numbers, which show the overall sales value was up: over 9% up on last year (according to Golf Datatech’s golf specialty audit). The love continued through the other categories: with 11 product groups showing an increase and 6 showing some decline.

Unsurprisingly, the biggest drop year on year was in Outerwear – down a massive 56%.

So what were the winners?

Amazingly, the top 7 categories all had increases, ranging from 2% for Shoes, to a whopping 28% for Men’s Shirts. The two big Hardware categories also saw double digit year-on-year growth. Balls were the 3rd largest growth category – up 22% on 2017.

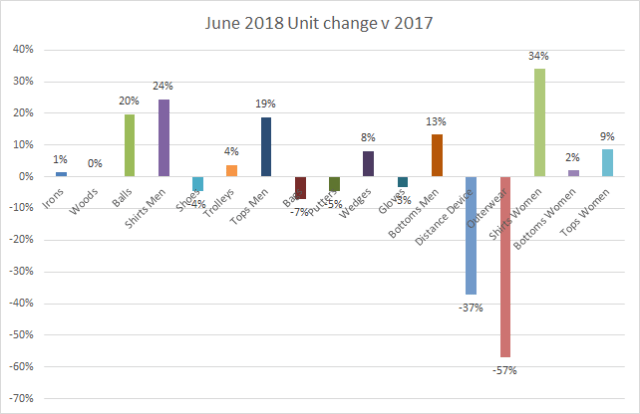

Was this all ASP growth? Or, did we actually sell more stuff?

More good news. Eleven categories saw a unit increase. The only category in the top 7 that saw growth in Value, but not in Units, was Shoes – seeing a 4% decline. Overall,

the main unit gains came in the classic summer categories of Balls and Shirts – both up over 20%. Interestingly, Ladies Shirts showed the biggest positive move – up 34% in units year on year. The other Ladies’ Apparel categories all followed suit – which is the first time in a while.

Unsurprisingly, ASP’s were up pretty much across the board. Irons led the way with a 20% increase year on year. Losses were negligible, with the worst category being Ladies Tops that dropped just over 4%.

Anything else of note?

Looking at the annual picture, June was actually quite a long way down on May this year. Normally, we see a drop of circa 3%: however, this year we saw a 7% decline month on month. Some of this might have been expected, as May was a very big month, (our biggest ever). In fact, taking another look at history, perhaps June 2018 performed exactly as expected. The bigger-than-normal decline could well be contributed to the Football World Cup. On average, we see a 5% bigger decline in June versus May in football championship years – which in this instance was pretty much spot on.

What is also interesting is how the month performed Vs last year, and the general weather picture. Last year, June was quite a weak month, with the second largest unit growth coming from Outerwear. Rain was higher then average, with 17% more rain days.

This June, by contrast, we only had 5 days with more than 1 mm of rain. It really was flaming June! This is incredibly low on the long term average of 11. With nearly 6 more golf days available than average this must have contributed to 35% increase in on-course golf Ball units sales year on year.

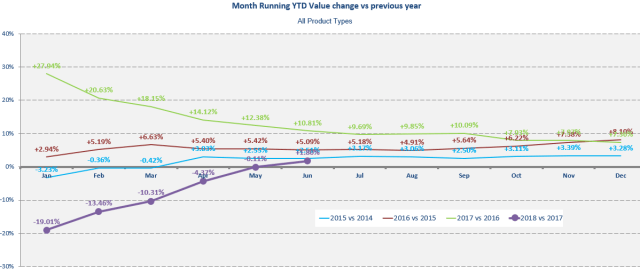

At the half-year point, what is the general thinking?

Looking at the year to date trends, we are now ahead of 2017 – something I didn’t think we would see this year. Year to date we are 1.8% up in value versus 2017.

Looking at our long-term trends, once we get to June, there is usually very little change in the annual overall position. Last year we saw a 3.5% decline June to December. In 2016, we saw a 3% growth over the same monthly period. Last year, we had a big Ping launch. That isn’t happening this year, but we do have some new Titleist products coming soon.

Gut feel is that we will see a bit of change year on year and I wouldn’t be surprised if we see a little softening in the numbers. June’s inventory figures showed that we are in a pretty healthy position, with stock levels lower than this time last year.

As a result there shouldn’t be massive pressure to run large sales too early. However, we have a Ryder Cup coming up, and if we get a good run of weather, then we could see the money continue to roll in. Fingers crossed it does!

For more information about Golf Datetech’s retail audit data covering all the key golf categories in the US, UK, Sweden, Germany and France contact Phil at pbarnard@golfdatatech.com