As we find ourselves in the depths of winter, it’s time to reflect on how the market performed in October, before sales start to drop off significantly.

October is often an unpredictable month. Usually the 7th largest of the year with around 8.3% of annual sales, and it can throw up some funny results. Some years, we see an “Indian Summer”, with extended periods of play. And on the other hand we could see an early start to the winter. It’s also a time when some brands launch new products but other retailers start major clearance. Needless to say it can throw out some spiky numbers.

So how did it go this year?

In the main, pretty bad compared to 2016. Overall sales value is 10.1% down on 2016 with some categories taking a significant drop. Looking at the overall breakdowns, the off-course clubs group was hit the hardest – seeing a 28.9% drop. In contrast, the on-course group saw a 13.7% increase. Other categories have not fared quite as well. Apparel, consumables and other categories are all down between 5.8% and 21.2%, both on- and off-course. The only category (outside of clubs) that is doing ok is light durables – held up by a strong showing from on course shoes.

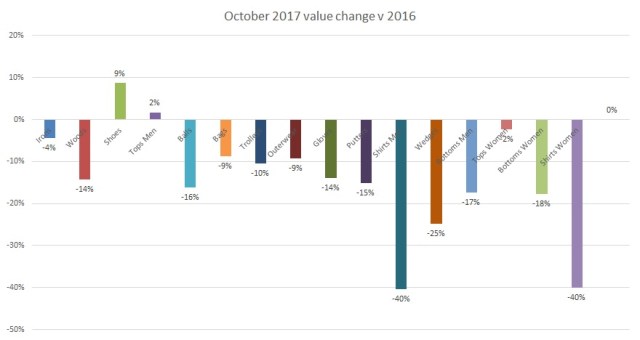

Looking at the total market for October, shoes and mens’ tops are the only categories to show any growth. Worst hit is shirts – both mens and ladies are down 40%

Was October a total disaster?

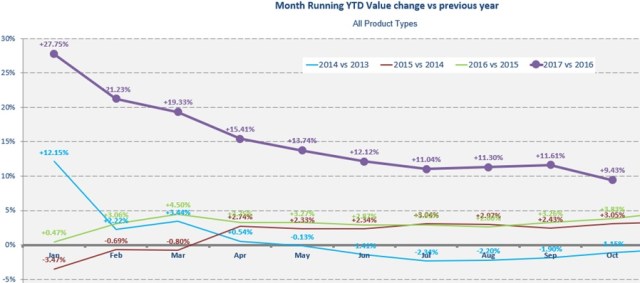

It would initially appear that way, but if you dive a little deeper into the numbers, it isn’t quite as clear as that. Even though this month’s values have seen a drop over last year, the year to date picture is still strong, with total sales value up 9.4%.

Compared to 2016, October was bad and there are a number of reasons for that. If we take a longer term perspective, October is only 1.6% down on 2015 … and actually 6.8% up in 2014. So when we look at this year’s performance, we need to consider that this October was “on-trend”, and that the real issue lies with a spike in the 2016 numbers.

Let’s compare stats for 2016 and 2017 for participation and weather

We don’t yet have any participation figures but we do know that this year, on-course ball sales were down 22.1% in units. This would indicate a significant drop in play. Looking at the weather stats, October started badly – hit by a couple of named storms that swept across from the US. However, looking at the rainfall and temperature, the UK actually had less rain than average – 90% – and the temperature was actually up 1.5% on average.

However, sunshine hours were only 80% of the long-term average. What is clear is that these figures are very different to 2016, which was a very good year, with only 42% of average rainfall and 119% of average sunshine hours. The other significant difference was in days of rainfall (a new stat that I have discovered – yeah!). October 2017 had 14 days of rain – one day under the average. 2016 only had 8! This lead to October 2016 seeing an increase in ball volume of 6.9% compared to 2017’s fall. Once the ’round-played’ stats come through, I am sure we will see a significant year-on-year drop-off in play.

So, is the weather to blame?

While undoubtedly the weather played its part, (it always does), this is only one part of the picture. The other major issue in the difference between 2016 and 2017 is the promotional activity run on the off-course last year. Last year saw a major push from the off-course channel for club business with some very aggressive promotions that lead to a 33.7% increase in off-course club sales. This is an unprecedented jump that probably had some longer term effects.

The promotion was so successful that it will have changed some consumers’ buying habits: bringing forward their normal purchase cycle.

So consumers who might have changed their irons every 6 years, had an incentive to trade-in their old clubs and get a new set a year, or two, early. This effectively brought forward some of this year’s sales.

The success of this promotion hasn’t been totally realised due to 2017’s successful product launches. Good showings from Ping and Titleist have hidden some of the disparity. On-course iron sales this month have shown a 37.4% increase on last year – a stellar performance and, in the main, reversing some of the channel shift that happened last year. On-course also saw some growth in woods. Overall these figures help support the clubs sales which overall saw drops between – 4% in irons to -24% in wedges.

Looking at the longer-term club trend, 2017 showed a 2.7% increase on 2015 and a 13% increase on 2014.

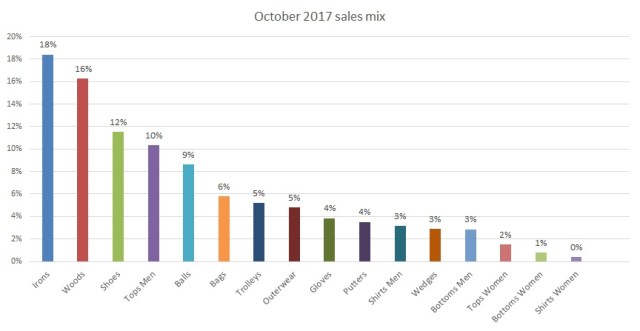

So, where did golfers spend their money?

For the first time in a while, we saw a change in the ranking of categories. Irons took top spot with 18%. The change in season brought some repositioning of the other categories, with mens’ tops and shoes jumping up the order, passed balls.

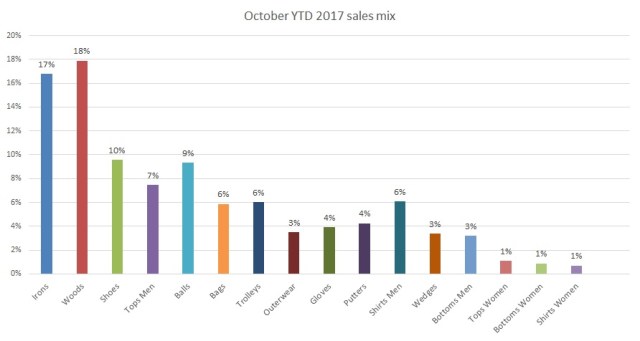

Looking at the year to date trends, you can see this a bit more clearly.

The main drop seen in shirts slipping down the order.

Drops in value were also mirrored with significant drops in volume this month.

Unless you were a shoe brand, this is probably one of the most depressing graphs I have seen in a long time. Shirts being the biggest loser, but generally everything getting a pounding. Let’s move on.

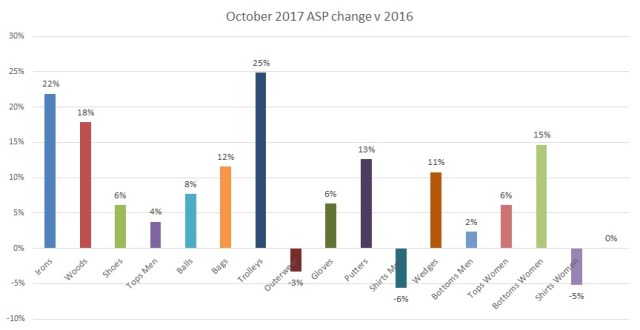

As we have seen all year ASP’s continue to rise and October is no different. Seeing considerable growth in 13 categories, with only 3 apparel categories seeing some single digit drops.

OK so with the exception of a relatively poor October most of the trends are the same as we have seen for most of this year. What next?

The big issue is whether the relative slump will continue. The worrying thing for me is that last year, October was 9.2% up on the previous year. November however was 17.2% up!! Based on this month’s trend, we might be in for a rocky month next month. Weather hasn’t been great to extend the season – unlike last year. We should also see further effects of last year’s off-course promotions, as they ran on for a couple of months. This is very likely to have an negative effect. Lets just hope the positive product launches can carry us on a bit further.

So where might we end up.

Earlier in the year, when sales were good, I tempered my enthusiasm for massive year on year growth – based on how strong the end of last season was. This seems to be coming true, with the steady year on year drop off continuing.

Having come from nearly 20% growth in March, its hard to think that this year’s gains might be relatively small. However the trend has declined in most months. As previously offered I was expecting something around 8% to 10% and I think that is still a possibility. While the boom of the last quarter in 2016 has had an effect on this year’s numbers, there have been some really strong product launches that continue to excite the consumer. Let’s hope they continue to buy with enthusiasm.