Its been a great year in the golf trade so far. Year on year, we see increases in participation and sales in nearly all categories that have EPOS systems ringing in the cash across the land. But is everyone a winner?

Both on and off course retailers have seen strong gains and shared the 15.4% YTD growth. On course was up 12.9% and off course was up 18.3% in value to the end of April. Greater participation than 2016 was highlighted with a more than 20% increase in April on course ball unit volumes – a good indication of play levels.

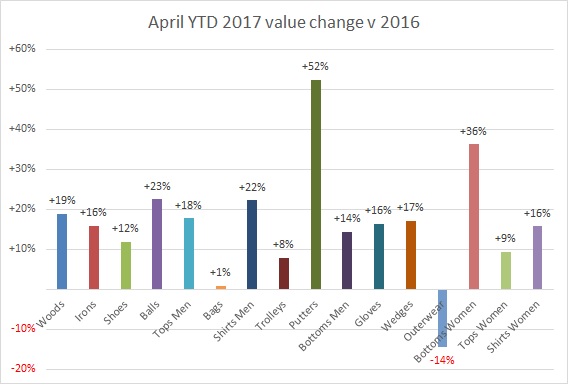

Is everything up?

Looking at the various categories everything was up except Outerwear – which has had a torrid time of late. Down 14% year to date, it has simply been too dry and too warm. I expect there are lots of apparel guys doing the rain dance!

Otherwise it was growth all round from the other categories in terms of value so far.

Bags have been the slowest – with a 1% gain and Putters have been the hottest, with an amazing 52% growth so far this year. With the exception of those two categories and Outerwear, the growth has been pretty consistent across the other categories, averaging 17%.

What is generating the most value?

I thought I would do something a bit different this month, and list which products generated the most value in the golf industry in April. Here they are:

In 5th place – FOOTJOY-Pro SL shoe

In 4th – PING-G Irons

In 3rd – TAYLORMADE-M2 17 Irons

In 2nd – CALLAWAY-GBB Epic Driver

And finally the product that generated the most revenue in the month of April was……

The Pro V1/x

Amazing to think with all that carbon, titanium and complex fabrics, that it is the very essence of the sport – a ball – that is taking the most money!

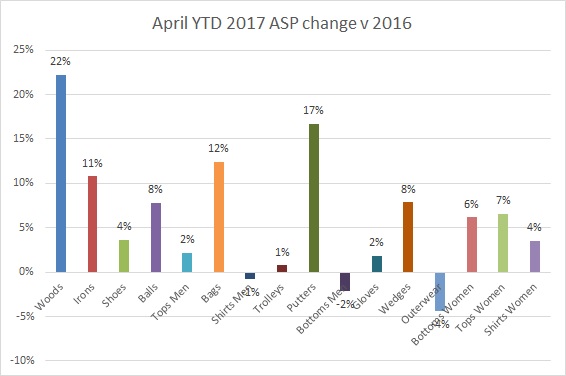

Values are up – is that down to pricing or volume?

Diving deeper in to the data, we can see that ASP has been a key driver in the value growth.

Woods – the biggest category has seen the largest change with + 22%. This is not just down to price increases, but has been driven by the hot new products in the category. Average ASP in woods for the end of 2016 was £168. So far this year, the average is over £200. The top 2 drivers – the TaylorMade M2 and Callaway Epic have been selling at over £320 and £420 respectively which has dragged up the average.

With a traditional supply and demand curve, we would expect there to be some drop off in units with an increase in cost.

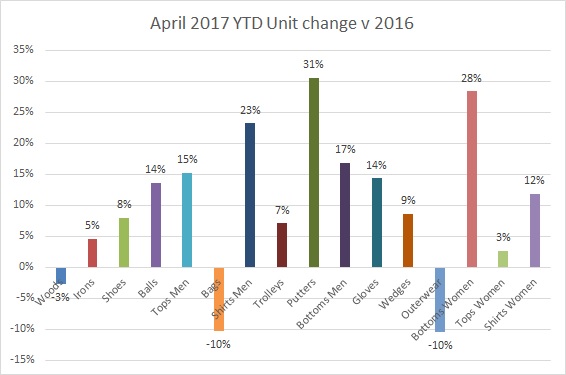

In woods that may be the case as we see the YTD units have dropped off by 3%. However in other categories, this hasn’t happened. In Putters, which had the second largest ASP jump of 17%, units are up 31%!

This is the case for many of the other categories. So all in all, this is good news for the trade. Higher prices and higher units going out of the store!

Is this trend going to continue?

I did buy a crystal ball recently but it didn’t come with instructions – so far its not telling me anything! However if you look at the historical data as an indicator, it shows us that once we get to the end of April, we will pretty much know where the year is going to end up. Assuming this year behaves the same as the last few years, it would be reasonable to assume that the year will end up circa +12 to 14% overall.

There are a couple of warnings ahead. Last year’s second half was stellar with lots of promotional activity. Its unlikely we can repeat that two years in a row. However there will most likely be a Ping launch later in the year (if they stick to normal release cycles) and that usually creates an up-kick. The only other thing to consider is the General Election and the fall out from that. With the level of uncertainty about the government and the countries direction – we could see a contraction in consumer spending that has a detrimental effect. Typically Golf is fairly well insulated from drastic changes and politics – so hopefully whatever the outcome, it won’t have too many negative effects.

Whatever happens, we will keep counting the numbers and keep you up to date with what’s going on.

All data supplied by the Golf Datatech retail audit. For more information contact me at pbarnard@golfdatatech.com