So how did the UK golf market perform in 2015? Here’s a quick overview…

For many it was up and down with various hits and misses across the product categories.

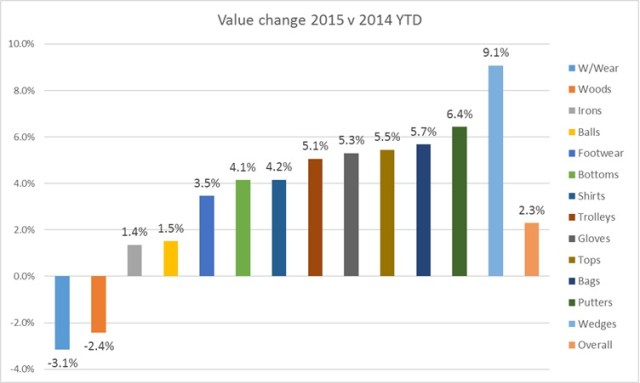

Overall it was positive with total sales up 2.3% – but before we break out the champagne lets look at things in a bit more detail. All categories except woods and outerwear experienced some growth. With the strongest category being Wedges up 9.1%

What has been interesting this year is the slight shift back to on course retail. On course is up 4.5% while the off course was down 0.6%. In the main this was down to the drop in hardware sales which affects the off course more significantly.

Generally the growth was driven by ASP – which is good. Sell things and sell them for more money. All categories saw a rise in average sales price – putters seeing the largest up 17%

Looking in detail its interesting to see what an increase some categories have had. Looking at the key market of woods in particular drivers. In 2015 – 4 of the top 6 drivers averaged over £240. In 2014 only 2 of the top 6 were in that price bracket.

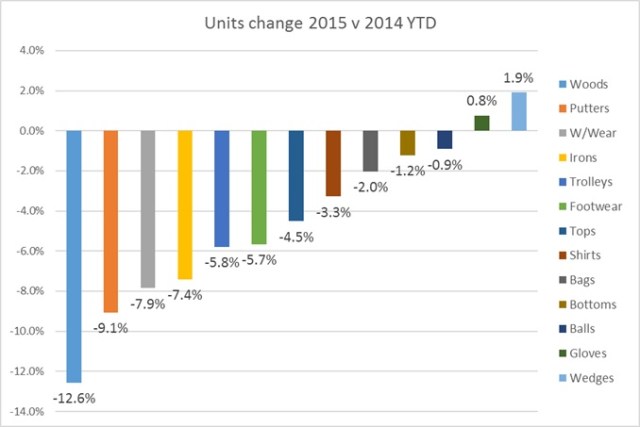

UNITS DOWN!!!

With ASP is up and up a lot in some categories this has had a negative effect on units. All categories except gloves and wedges saw a fall. Woods were down 12.6% overall.

Is this the effect of higher prices or were less units driven as less promotion was taking place – keeping prices up? In some categories I think there was a definite move away from promotion with less clearance going on in the hardware categories and an effort to keep up asp and hopefully margin. Its interesting to see that 3 of the 4 worst performing categories were hardware. Perhaps this is also an indication of changing life cycles with custom fit.

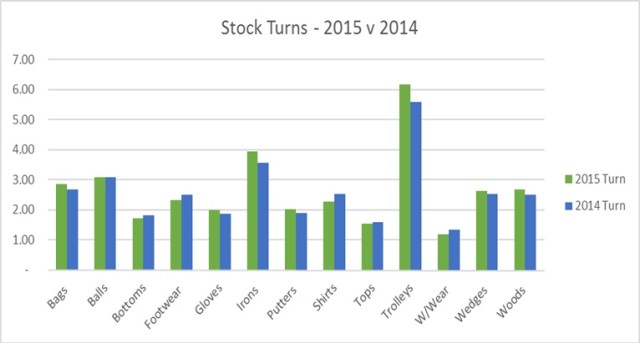

Stock

Final area to comment on is the stock situation. Like ASP, stock turn was generally up across the industry. However there was a clear trend split in hardware v soft goods.

Hardware improved stock turn – with everything turning quicker in 2015. Custom fit has definitely helped in this area. However apparel had a bit of a shocker with all categories except shirts seeing turns of less than 2 and a decline since 2014. Last years strong apparel sales seems to have caught everyone out. In general we are over stocked in clothing.

Overall the industry was running at 2.6 turns at the end of the year. Better than 2014 but still too low. We should be aiming for 3.5 – this would help cash and help margins.

… and next year?

Its always tough to call what is going to happen. We are so dependent on the weather – which I know people don’t like but that is the way it is! If we get a good March/April then we should get a good season.

What I can say is that we should expect to see some decline as a result of the football championships and Olympics in the summer. Historically they have produce a circa 5% decline or so.

Generally I would hope to see a bit of a shift in hardware. Woods might buck the recent trend of decline with some new products from all manufacturers hopefully creating some reason to buy.

What will also be interesting to see is how the off course reacts following a slightly disappointing year. I expect to see some reaction as they aim to get back some market share.

However it goes – I hope its a good one and you can be sure that we will have all the data to keep everyone informed of the progress.