Time seems to have run away with me this month. As I prepare for the July figures to be processed I realise that I haven’t written an analysis for June. So before we get ahead of ourselves here goes.

June was a bit of a funny month on the weather front. Colder than the long term average with a smattering of gales and rain, then finished off with a heatwave. Fortunately rain fall was less than average (-25%) – which always helps participation on the course.

Participation appears to have been similar to last year with ball unit sales being just 0.6% down on 2014 and glove sales being up 5%

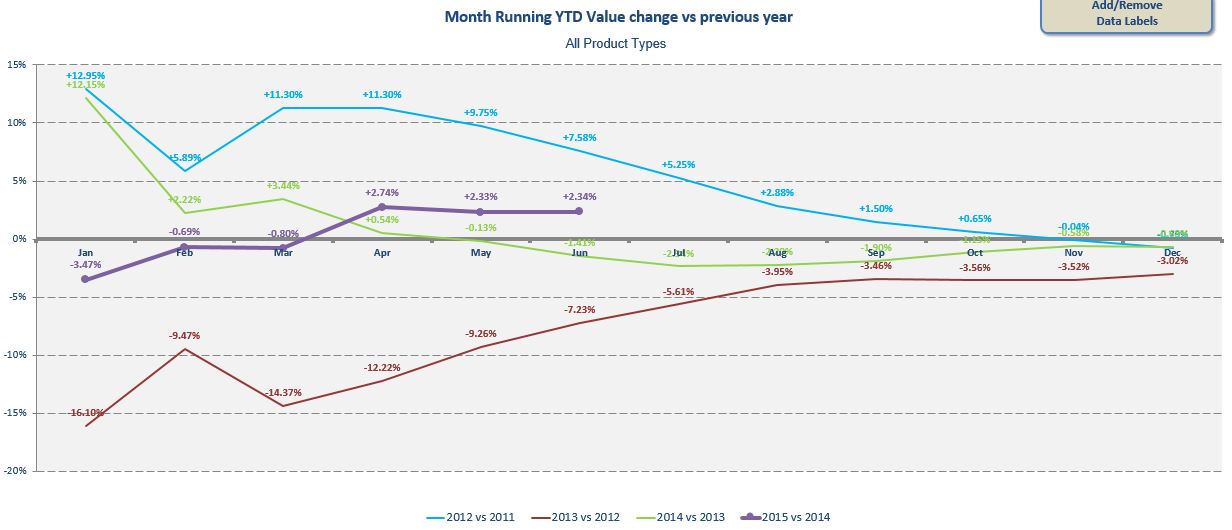

Overall result for June shows retail was up 2.4% in value leading to a year to date increase for 2015 of 2.3% – a positive trend in value terms. Here is a graph to show you how these figures compare for the last few years. Click on the graph to enlarge.

So positive value for the market overall. So where has this growth come from?

In the main is apparel and non club products. With the exception of weather wear all the clothing categories are up 5%+, trolleys, bags and gloves are showing similar or better growth. This should be good news for retailers as most of these products deliver good margin. As mentioned previously – most of this growth is coming from increased ASP. Units seem to be down or flat in all categories other than gloves.

Hardware seems to be doing worst, with all categories except wedges down by more than 6% in unit terms for June – with a similar story for the year to date.

June saw an ASP increase for all categories and all channels – except for on course weather wear – but 25 out of 26 tracked markets is pretty good. Putters set the pace for the largest growth – nearly 15% v 2014.

The reduction in unit sales has also come with a healthy reduction in inventory across the industry. This is a really positive thing. The industry has become chocked with stock over the last few years with on course stock turns dropping from 2.4 a few years ago to 2 or less last year. Too much stock leads to too much clearance which means to price reductions and reduced value for consumers and retailers.

A shift to slightly longer product cycles with allow the industry to manage the retail proposition better – in the long run everyone gets more value.

Lets hope the positive trends carry on with July and August.